|

|

|

Одним из пионеров метода VSA был Ричард Д. Вайкофф (Wyckoff). Первая инструкция Ричарда Вайкоффа студентам, изучающим его метод анализа акций, опубликованный в тридцатых годах прошлого века, была совершенно простой и определенной - забыть все когда-либо используемые факторы принятия решений. Все, что вам нужно знать, находится в таблице цен и объемов акций в вашей ежедневной газете. С таким подходом возврата к основам Вайкофф обещал показать своим студентам "настоящие правила игры", в которую так ловко играют состоятельные инвесторы с достаточным капиталом на рынке. Несмотря на то, что трудно представить себе что-либо, особенно технику фондовой биржи, остававшееся жизнеспособным с тридцатых годов до настоящего времени, "Метод Торговли и Инвестирования в Акции" Ричарда Вайкоффа прошел сквозь времена, став классикой. Хотя в наше компьютеризированное время не ощущается недостатка в волшебных методиках, техника Вайкоффа дает твердую базу для анализа фундаментальных взаимоотношений среди первоначальных сил рынка. Вайкофф был заинтригован фондовой биржей. Он изучал рынок снизу доверху, когда только опыт мог быть единственным учителем. Его первой работой в 1888 году, в 15-летнем возрасте, было разносить акции, носясь взад и вперед по Уолл-стрит, доставляя и обменивая ценные бумаги и платежи для брокерской фирмы. К 1898 году он продвинулся до аудитора другой брокерской фирмы и дал свои первые $1,000 прибыли на рынке акций, продав 300 акций компании, выпустившей новый продукт - пневматический конный ошейник. В возрасте 25 лет он открыл собственный брокерский офис. Он видел "бешеные убытки на ценных бумагах, которые ежегодно несут миллионы людей, не осознающих величину своего риска и имеющих поразительно малые знания о рынке". Он отправлял своим клиентам ежедневные письма о состоянии рынков, занимаясь исследованиями и публикациями в ежемесячном журнале в 1907 году. Будучи брокером, он видел закулисные игры крупных спекулянтов и понимал, "что есть возможность оценить будущий курс рынка по его собственным действиям ... что действия акций отображает планы и цели тех, кто доминирует над ними ... что основной закон предложения и спроса управляет всеми изменениями цен; что лучший индикатор будущего курса рынка - отношение спроса к предложению". Вайкофф опубликовал свой первый метод технического анализа в 1908 году, а в 1911, по настойчивым просьбам читателей, начал публиковать еженедельные прогнозы, используя для анализа графики движений цены и объема. Относящиеся с пренебрежением к Вайкоффу аналитики использовали графики в качестве своего рода теста Роршаха, в поисках формаций, которые сигнализировали бы о покупке, продаже или удержании. "Техника рынка акций не является точной наукой", говорил он своим студентам. "Цены акций делаются мозгами людей". По его мнению, механический или же исключительно математический анализ графика не может конкурировать с тщательно продуманным суждением. Вайкофф также избегал финансовых отчетов, новостей, отчетов о доходах и особенно слухов, подсказок и "полусырых торговых теорий, изложенных в популярных книгах о рынке".

|

|

Добрый день, Господа! Начинаем блог анализа движения цены и объемов (Volume Spread Analysis) американских акций. Вначале я кратко изложу теоретическую часть метода, а с мая планирую писать ежедневные обзоры с торговыми рекомендациями.

|

|

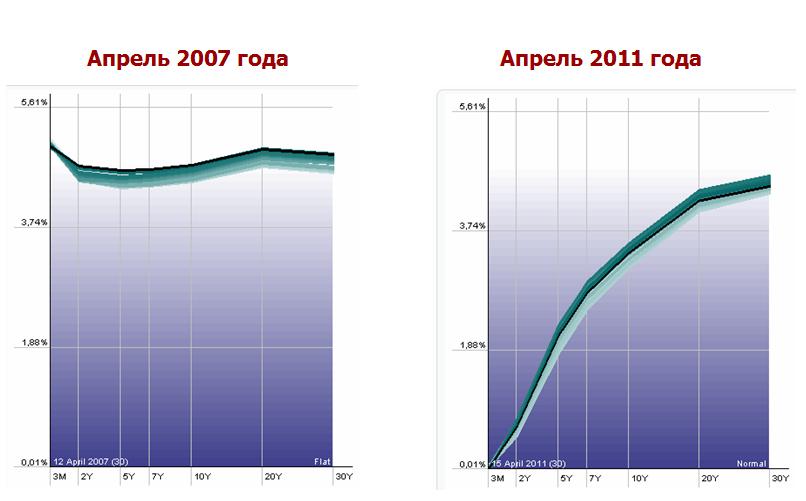

Вчера после того, как агентство S&P объявило о снижении прогноза суверенного рейтинга США, US Treasures повели себя странно – они стали расти. Это правда неестественно: доверие к стране снижается, а ее ценные бумаги с фиксированной доходностью при этом растут. Возникает какое-то новое поведение, которое хочется как-то объяснить. Не меня одного это удивило. Известный блоггер и экономист Paul Krugman из New York Times написал по этому поводу следующее: I think the financial press is being even denser than usual on this one. If S&P warns that US bonds might not be safe, and the price of those bonds rises, you really have to wonder how anyone can write with a straight face that this warning caused other market movements. And it’s much worse to have this implausible theory reported as a settled fact. Малоубедительное объяснение предложил Блумберг: Treasury’s Oldest Bonds Show Demand as End of QE2 Nears April 18 (Bloomberg) — Investors are paying the smallest discounts for Treasuries other than the newest, most-traded bonds since the start of the financial crisis, a sign of growing demand even as the Federal Reserve’s $600 billion buying program approaches its conclusion. Yields on older notes with 10 years left to maturity have fallen to within 11.4 basis points, or 0.114 percentage point, of those on the newest securities of the same maturity, down from the peak of 66.1 in January 2009, according to data from Barclays Plc. The gap for so-called off-the-run notes narrowed to as little as 6.6 basis points in February, the least since May 2007. Так выглядят 10-летние US Treasures

Может быть дело в техническом факторе? Поскольку торгуются в верхних 38% обоих размахов? Что-то определенно скрывается за этим движением (обычно US Treasuries росли в период ожидания QE). Очень любопытная статья появилась сегодня на Блумберге. April 19 (Bloomberg) -- Federal Reserve Chairman Ben S. Bernanke may keep reinvesting maturing debt into Treasuries to maintain record stimulus even after making good on a pledge to complete $600 billion in bond purchases by the end of June. The Fed chief’s top two lieutenants said this month the economy and inflation are too weak to warrant the start of a monetary-policy reversal. Investors and economists including David Kelly at JPMorgan Funds see that as a signal the Fed will keep its balance sheet at current levels by replacing about $17 billion a month in maturing mortgage debt with Treasuries. Ending the reinvestment policy and the $600 billion program at the same time would be like quitting stimulus “cold turkey,” said Kelly, who is based in New York and helps oversee $400 billion as chief market strategist at JPMorgan. “It does make sense to reinvest for a while,” he said. “Then they could watch how bond yields react to that.” Два адъютанта его превосходительства главы Феда (имеются в виду два его зама – Уильям Дадли и Джанет Йеллен) заявили в этом месяце, что экономика и инфляция еще слишком слабы, чтобы гарантировать начало разворота в монетарной политике. Инвесторы и экономисты видят сигналы, что Фед сохранит баланс на прежнем уровне, реинвестируя ежемесячно 17 млрд. долларов ипотечного долга в казначейские облигации. На трейдерском жаргоне это называется QE Lite. Заявлено между прочим достаточно уверенно и я бы даже сказал - безапелляционно. Похоже на сознательную утечку. После понижения прогноза рейтинга, а есть мнение, что было сделано это с подачи монетарных властей США и крупные игроки знали об этом еще в пятницу (смотрим, когда начали расти облигации) видимо было принято решение о реинвестировании и теперь Блумберг доносит его до нас. Вчера перед нами разыграли спектакль! Это позитивная новость для рынков. Возможно, об этом объявят на заседании ФОМС 27 апреля. Но это не снимает вопроса: за счет чего будет финансироваться дефицит бюджета. Вот, кажется, нашлось объяснение такого поведения US Treasures.

|

|

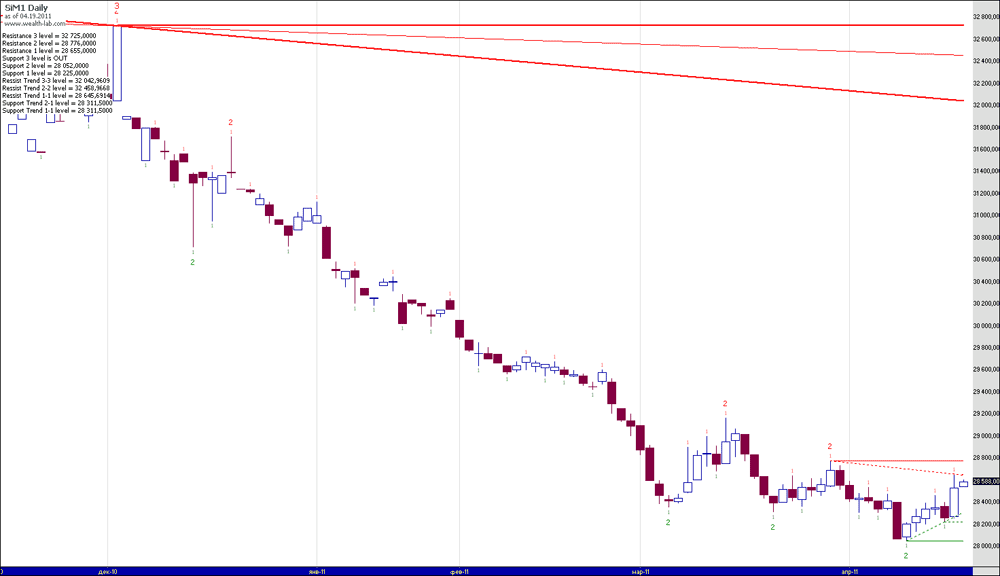

Сегодня, 19.04.11, если цены будут повышаться, то я буду покупать фьючерсы ED-06.11, RTS-06.11, VTBR-06.11, SBRF-06.11, GAZR-06.11, ROSN-06.11, LKOH-06.11. Если цены будут понижаться, то я буду продавать акции СевСт-ао и фьючерсы Si-06.11 по 28299. Торги акциями ГАЗПРОМ, Сургнфгз, Роснефть, ГМКНорНик, ВТБ, ФСК ЕЭС, Сбербанк, РусГидро, ЛУКОЙЛ и фьючерсами GOLD-06.11, Eu-06.11, GMKR-06.11 запрещены из-за экстремальной волатильности инструментов.

|

|

Сегодня будет как обычно три прогноза. ПРОГНОЗ ОТ МЕХАНИЗАТОРА С САЙТА RUSSIAN-TRADER.RU Локальная коррекция, начавшаяся на рынках в понедельник, с выходом новости от S&P переросла в панические продажи. Движение поломало всю техническую картинку, Штаты обновили дно прошлой недели, а наш рынок, и без того слабый, укатали вниз почти на 4% по индексу ММВБ. Впрочем, мы закрылись на пике негатива, уже к ночи Штаты пошли на восстановление, утро у нас можно ожидать с гэпами вверх. Сложно сказать, насколько быстро эмоции вокруг новости улягутся, по факту ничего нового не случилось, вряд ли информация о проблемах в Штатах для кого-то явилась откровением, но настроение инвесторам, тем не менее, испортили, что скажется. Все таки лучше не ловить отскок во вторник, на всякий случай. Рынки будут искать более-менее стабильный уровень, трейдеры будут определяться с настроением под дальнейшее движение. Распилить может в обе стороны. ПРОГНОЗ ОТ ЧЕССПЛЕЙЕРА На прошлой неделе было самое крупное недельное снижение российского рынка, а вчера, наверно, одно из самых крупных дневных снижений с того времени. Эту неделю мы начали очень достойно; как всегда летим впереди всех. Об этом, кстати, я еще писал во вью российский рынок сегодня 13 апреля Как я и предполагал, вчерашний гэп так и не был закрыт и падение оказалось довольно сильным: 2.5%. Зато почти закрыли другой гэп – противоположный от 29 марта и наш рынок дошел почти до верхней границы январско-мартовской консолидации. Это говорит о том, что крупняк выходит, и покупателей практически нет. Это существенно меняет ориентиры для нынешнего падения: теперь это уже 1680 пунктов по индексу ММВБ, и учитывая то, как мы любим бежать впереди паровоза, достигнуты они могут быть на удивление быстро. А в принципе для нас меньше всего оснований для распродаж, поскольку у нашей страны на самом деле очень сильный БАЛАНС, о значении которого пишет Bob Janjuah Очень заманчиво откорректироваться до нижней границы январско-мартовского диапазона (уровень 1670-1680 )уже сегодня-завтра – осталось так немного. Нефть будет этому сегодня способствовать, а вот американский фьюч - скорее всего нет. Наиболее вероятным мне кажется сегодня боковик чуть выше вчерашнего закрытия. ПРОГНОЗ ОТ ВАНУТЫ С КВОТФОРУМА Амеры в целом торговались неплохо, пока ближе к их открытию не появилась новость от агентства "стандартные и бедные", возжелавшее поучаствовать в шантаже конгресса, в котором не могут разобраться с дефицитом бюджета и верхней планкой госдолга, и изменило прогноз рейтинга США со "стабильного" на "негативный", причем решение агентства стало неожиданным для рынков, хотя всем понятно, что оно возникло по воле конкретных лиц, и раз министерство финансов США высказало "удовлетворение" этим решением, то было еще и санкционировано на высшем уровне. Сам рейтинг у США не изменялся с 1941 года, и не будет изменен, чтобы не произошло, это понятно и ежикам в пампасах, насилующих кактусы. И поэтому понижение прогноза на рейтинг в будущем превратится в бычий сигнал, когда отыграют все назад. Все рынки на это среагировали эмоциональнее, чем сами амеры, особенно наш фырик, в котором уже были набраны правильные шорты и крупные спекули только и ждали какой-нибудь негативной новости. В итоге ММВБ рухнула под -4%, давненько я не видел как ГП на -10 рублей за полчаса падает (провалился аж до 217, -30 рублей от хаев года в 247.7, вертикально, без отскока больше чем на два рубля - вот что значит полностью манипулировать нашим рынком, вертикально +30 и сразу вертикально -30 рублей сыграли, а кукловодов как не было, так и нет, что вы, абсолютно рыночные движения))). В итоге сегодня напрашивается день отскока, это слишком очевидно, и поэтому возможно днем попробуют снова залить наш рынок, но в целом думается что амеры выкупятся, 1290 (цель этой недели) они уже показали, и на такой лаже как решение карманного агентства, можно только покупать на их рынке, а не продавать. В итоге утром нейтрально, на полпроцента вверх, потом снова скорее всего придавят к 1705-1710, и начнут откупаться ползучим восходящим образом. Это если сегодня начнут откупать "правильные" шорты.

|

|

Доброе утро, господа, и удачного вам дня! Вью рынка от 19 апреля 2011 года. Вчера утром пришли две новости – обе негативные: одна из Финляндии о результатах выборов и какие проблемы это создаст для еврозоны ( об этом я писал на блоге), вторая из Греции. На уровне утечки информации стало известно, что, оказывается, еще в начале апреля Греция передала запрос о реструктуризации своих долгов. Процесс переговоров будет запущен в июне месяце. На этих двух новостях евро стал сильно распродаваться, европейские рынки снижаться и тянуть за собой всех остальных, а облигации периферийной еврозоны ставить новые рекорды доходности. Вечером добавилась еще одна негативная новость, теперь уже из Америки: агентство S&P понизило прогноз суверенного рейтинга США со стабильного на негативный. В этой новости на самом деле тоже не было ничего такого серьезного: прогноз это же не сам рейтинг. С самим рейтингом если что-то произойдет, то очень-очень нескоро. Суть в том, что совершенно непонятна ситуация с бюджетом на 2012, и потолок госдолга они не спешат увеличивать, и это уже начинает вызывать нервозность. Из инсайдерских источников того же S&P между участниками переговоров неразрешимые противоречия. На самом деле, вчерашняя коррекция на мой взгляд не связана непосредственно с этими событиями; с таким же успехом она могла случиться и в пятницу и отражает смену рекомендаций некоторых очень мощных, аффилированных с монетарными властями США, финансовых структур. Голдман сказал - падать? Значит будем падать! Цены стали якобы чересчур высокие (для нынешней ситуации это неправда). Но нынешний механизм монетарной политики, который я описал здесь , уже не остановить, следовательно мы увидим еще более высокие цены. Чем больше ФРС покупает US Treasuries, тем больше становятся резервы крупнейших мировых финансовых институтов и тем выше ликвидность. Таков механизм, и нет никаких признаков, что Фед собирается что-то менять. Тем не менее коррекция, срежиссированная стратегами Goldman Sachs, еще далека от завершения; на мой взгляд ее цели где-то в районе 1250 или 1230 пунктов. Но каким будет маршрут и расписание движения – сказать трудно. Сейчас мне кажется более вероятным сначала отскок американского фьюча S&P500 в район 1310-1315 пунктов, или даже выше, а уже затем продолжение снижения. Несколько странно ведут себя US Treasures; на всех этих новостях о понижении прогнозов они должны падать, а они растут. Возможно, причина в сильной корреляции в текущий момент с индексом доллара, либо это искусственный процесс. В ближайшее время мы это узнаем.

|

|

Из известных людей первой реакция пришла от Mohamed El-Erian, chief executive and co-chief investment officer at PIMCO S&P reaffirmed this morning the AAA rating of the US but, importantly, slapped a “negative outlook” on the rating due to concerns on how the country will address its “very large budget deficits and rising government indebtedness.” In justifying this dramatic move, it noted that “there is a material risk that US policymakers might not reach an agreement in how to address medium- and long-term budgetary challenges by 2013.” This is a timely reminder of the seriousness of America’s fiscal issues, for the country and for the rest of the world. The continued failure to come up with a credible medium-term fiscal reform program would increase borrowing costs for all segments of US society, thereby undermining investment, employment and growth. It would also curtail foreigners’ appetite to add to their already substantial holdings of US assets. And it would weaken the dollar. The US also risks eroding its standing at the core of the global monetary system. The world looks to America for a range of “global public goods” — including the reserve currency, the deepest and most liquid government debt markets, and the “risk free” standard. With no other country able and willing to step into this role, the result would be global efficiency losses and a higher risk of economic and financial fragmentation. S&P’s warning should be heard loud and clear in Washington DC, hopefully acting as a catalyst for faster convergence on a credible medium-term fiscal package. It is also a reminder of risk to the global economy, as well as the generalized deterioration in the sovereign credit quality of several advanced economies. The time has come for the US (and other advanced economies) to take better control of its fiscal destiny—for the sake of American society and for the well being of the global economy. А вот что думает об этом уже известный нам Bob Janjuah: Перестаньте беспокоиться о еврозоне и ее периферии и начинайте беспокоиться о США ( долларе). Вот что он написал: Glad I put my note out last week. Folks way too focused on eurozone, where ORDERLY restructuring of greece and maybr too ireland and port, and meaningful fiscal adjustment, are both part of the l-t credible solution and where acceptance of this is a good thing in the long run as it means the euro and ECB are credible and not at risk of fiat money printing. At the other end we have the US where the mrkt is way way too complacent abt the fast deteriorating credit risk of USA Inc., and where the hope for credible and meaningful fiscal adjustments are a mere dream, and where we have a central bank that knows only 1 (failed) trick – money debasement. А вот что сообщает инсайдер от Рейтерс S&P GLOBAL SOVEREIGN RATINGS HEAD SAYS NEITHER OBAMA NOR REP. RYAN PLAN ENOUGH TO FIX DEFICIT– REUTERS INSIDER S&P GLOBAL SOVEREIGN RATINGS HEAD SAYS GULF BETWEEN U.S. PARTIES ON DEFICIT PLAN HAS NEVER BEEN WIDER– REUTERS INSIDER S&P GLOBAL SOVEREIGN RATINGS HEAD SAYS RISK IS U.S. RATING COULD FALL TO AA+ FROM AAA– REUTERS INSIDER S&P GLOBAL SOVEREIGN RATINGS HEAD SAYS U.S. DOLLAR WELL ENTRENCHED AS WORLD RESERVE CURRENCY, WILL BE SLOW TO CHANGE– REUTERS INSIDER Ни Обама ни республиканец Райан не имеют плана, чтобы зафиксировать дефицит Никогда пропасть между двумя политическими партиями относительно бюджетного дефицита не была столь широка Рейтинг США может упасть до АА+ Роль доллара, который застолбил за собой место мировой резервной валюты, будет меняться Но мне все-таки непонятно, почему доллар рос после этой новости относительно всех валют (не только евро) и американские облигации продолжают расти (доходность падает)?

|

|

Событием, которое так взбудоражило рынки, стал пересмотр рейтинговым агентством США прогноза суверенного рейтинга США Агентство S&P пересмотрело прогноз суверенного рейтинга США на негативный От агентства S&P We have affirmed our 'AAA/A-1+' sovereign credit rating on the United States of America. - The economy of the U.S. is flexible and highly diversified, the country's effective monetary policies have supported output growth while containing inflationary pressures, and a consistent global preference for the U.S. dollar over all other currencies gives the country unique external liquidity.

- Because the U.S. has, relative to its 'AAA' peers, what we consider to be very large budget deficits and rising government indebtedness and the path to addressing these is not clear to us, we have revised our outlook on the long-term rating to negative from stable.

- We believe there is a material risk that U.S. policymakers might not reach an agreement on how to address medium- and long-term budgetary challenges by 2013; if an agreement is not reached and meaningful implementation does not begin by then, this would in our view render the U.S. fiscal profile meaningfully weaker than that of peer 'AAA' sovereigns.

Что это означает The negative outlook on our rating on the U.S. sovereign signals that we believe there is at least a one-in-three likelihood that we could lower our long-term rating on the U.S. within two years. The outlook reflects our view of the increased risk that the political negotiations over when and how to address both the medium- and long-term fiscal challenges will persist until at least after national elections in 2012. Негативный прогноз означает, что агентство полагает, что существует вероятность один к трем, что в течении ближайших двух лет агентство понизит рейтинг США. В принципе ничего особенного. Объяснение (они написали то, что уже давно было понятно всем) Our ratings on the U.S. rest on its high-income, highly diversified, and flexible economy, backed by a strong track record of prudent and credible monetary policy. The ratings also reflect our view of the unique advantages stemming from the dollar's preeminent place among world currencies. Although we believe these strengths currently outweigh what we consider to be the U.S.'s meaningful economic and fiscal risks and large external debtor position, we now believe that they might not fully offset the credit risks over the next two years at the 'AAA' level. The U.S. is among the most flexible high-income nations, with both adaptable labor markets and a long track record of openness to capital flows. In addition, its public sector uses a smaller share of national income than those of most 'AAA' rated countries--including its closest peers, the U.K., France, Germany, and Canada (all AAA/Stable/A-1+)--which implies greater revenue flexibility. Furthermore, the U.S. dollar is the world's most used currency, which provides the U.S. with unique external flexibility; the vast majority of U.S. trade flows and external liabilities are denominated in its own dollars. Recent depreciation of the currency has not materially affected this position, and we do not expect this to change in the medium term (see "Après Le Déluge, The U.S. Dollar Remains The Key International Currency," March 10, 2010, RatingsDirect). Despite these exceptional strengths, we note the U.S.'s fiscal profile has deteriorated steadily during the past decade and, in our view, has worsened further as a result of the recent financial crisis and ensuing recession. Moreover, more than two years after the beginning of the recent crisis, U.S. policymakers have still not agreed on a strategy to reverse recent fiscal deterioration or address longer-term fiscal pressures. In 2003-2008, the U.S.'s general (total) government deficit fluctuated between 2% and 5% of GDP. Already noticeably larger than that of most 'AAA' rated sovereigns, it ballooned to more than 11% in 2009 and has yet to recover. On April 13, President Barack Obama laid out his Administration's medium-term fiscal consolidation plan, aimed at reducing the cumulative unified federal deficit by US$4 trillion in 12 years or less. A key component of the Administration's strategy is to work with Congressional leaders over the next two months to develop a commonly agreed upon program to reach this target. The President's proposals envision reducing the deficit via both spending cuts and revenue increases, and the adoption of a "debt failsafe" legislative mechanism that would trigger an across-the-board spending reduction if, by 2014, budget projections show that federal debt to GDP has not yet stabilized and is not expected to decline in the second half of the current decade. The Obama Administration's proposed spending cuts include reducing non-security discretionary spending to levels similar to those proposed by the Fiscal Commission in December 2010, holding growth in base security (excluding war expenditure) spending below inflation, and further cost-control measures related to health care programs. Revenue would be increased via both tax reform and allowing the 2001 and 2003 income and estate tax cuts to expire in 2012 as currently scheduled--though only for high-income households. We note that the President advocated the latter proposal last year before agreeing with Republicans to extend the cuts beyond their previously scheduled 2011 expiration. The compromise agreed upon in December likely provides short-term support for the economic recovery, but we believe it also weakens the U.S.'s fiscal outlook and, in our view, reduces the likelihood that Congress will allow these tax cuts to expire in the near future. We also note that previously enacted legislative mechanisms meant to enforce budgetary discipline on future Congresses have not always succeeded. Key members in the U.S. House of Representatives have also advocated fiscal tightening of a similar magnitude, US$4.4 trillion, during the coming 10 years, but via different methods. House Budget Committee Chairman Paul Ryan's plan seeks to balance the federal budget by 2040, in part by cutting non-defense spending. The plan also includes significantly reducing the scope of Medicare and Medicaid, while bringing top individual and corporate tax rates lower than those under the 2001 and 2003 tax cuts. We view President Obama's and Congressman Ryan's proposals as the starting point of a process aimed at broader engagement, which could result in substantial and lasting U.S. government fiscal consolidation. That said, we see the path to agreement as challenging because the gap between the parties remains wide. We believe there is a significant risk that Congressional negotiations could result in no agreement on a medium-term fiscal strategy until after the fall 2012 Congressional and Presidential elections. If so, the first budget proposal that could include related measures would be Budget 2014 (for the fiscal year beginning Oct. 1, 2013), and we believe a delay beyond that time is possible. Standard & Poor's takes no position on the mix of spending and revenue measures the Congress and the Administration might conclude are appropriate. But for any plan to be credible, we believe that it would need to secure support from a cross-section of leaders in both political parties. If U.S. policymakers do agree on a fiscal consolidation strategy, we believe the experience of other countries highlights that implementation could take time. It could also generate significant political controversy, not just within Congress or between Congress and the Administration, but throughout the country. We therefore think that, assuming an agreement between Congress and the President, there is a reasonable chance that it would still take a number of years before the government reaches a fiscal position that stabilizes its debt burden. In addition, even if such measures are eventually put in place, the initiating policymakers or subsequently elected ones could decide to at least partially reverse fiscal consolidation. In our baseline macroeconomic scenario of near 3% annual real growth, we expect the general government deficit to decline gradually but remain slightly higher than 6% of GDP in 2013. As a result, net general government debt would reach 84% of GDP by 2013. In our macroeconomic forecast's optimistic scenario (assuming near 4% annual real growth), the fiscal deficit would fall to 4.6% of GDP by 2013, but the U.S.'s net general government debt would still rise to almost 80% of GDP by 2013. In our pessimistic scenario (a mild, one-year double-dip recession in 2012), the deficit would be 9.1%, while net debt would surpass 90% by 2013. Even in our optimistic scenario, we believe the U.S.'s fiscal profile would be less robust than those of other 'AAA' rated sovereigns by 2013. (For all of the assumptions underpinning our three forecast scenarios, see "U.S. Risks To The Forecast: Oil We Have to Fear Is...," March 15, 2011, RatingsDirect. Additional fiscal risks we see for the U.S. include the potential for further extraordinary official assistance to large players in the U.S. financial or other sectors, along with outlays related to various federal credit programs. We estimate that it could cost the U.S. government as much as 3.5% of GDP to appropriately capitalize and relaunch Fannie Mae and Freddie Mac, two financial institutions now under federal control, in addition to the 1% of GDP already invested (see "U.S. Government Cost To Resolve And Relaunch Fannie Mae And Freddie Mac Could Approach $700 Billion," Nov. 4, 2010, RatingsDirect). The potential for losses on federal direct and guaranteed loans (such as student loans) is another material fiscal risk, in our view. Most importantly, we believe the risks from the U.S. financial sector are higher than we considered them to be before 2008, as our downward revisions of our Banking Industry Country Risk Assessment (BICRA) on the U.S. to Group 3 from Group 2 in December 2009 and to Group 2 from Group 1 in December 2008 reflect (see "Banking Industry Country Risk Assessments," March 8, 2011, and "Banking Industry Country Risk Assessment: United States of America," Feb. 1, 2010, both on RatingsDirect). In line with these views, we now estimate the maximum aggregate, up-front fiscal cost to the U.S. government of resolving potential financial sector asset impairment in a stress scenario at 34% of GDP compared with our estimate of 26% in 2007. Beyond the short- and medium-term fiscal challenges, we view the U.S.'s unfunded entitlement programs (such as Social Security, Medicare, and Medicaid) to be the main source of long-term fiscal pressure. These entitlements already account for almost half of federal spending (an estimated 42% in fiscal-year 2011), and we project that percentage to continue increasing as long as these entitlement programs remain as they currently exist (see "Global Aging 2010: In The U.S., Going Gray Will Cost A Lot More Green," Oct. 25, 2010, RatingsDirect). In addition, the U.S.'s net external debt level (as we narrowly define it), approaching 300% of current account receipts in 2011, demonstrates a high reliance on foreign financing. The U.S.'s external indebtedness by this measure is one of the highest of all the sovereigns we rate. While thus far U.S. policymakers have been unable to agree on a fiscal consolidation strategy, the U.S.'s closest 'AAA' rated peers have already begun implementing theirs. The U.K., for example, suffered a recession almost twice as severe as that in the U.S. (U.K. GDP declined 4.9% in real terms in 2009, while the U.S.'s dropped 2.6%). In addition, the U.K.'s net general government indebtedness has risen in tandem with that of the U.S. since 2007. In June 2010, the U.K. began to implement a fiscal consolidation plan that we believe credibly sets the country's general government deficit on a medium-term downward path, retreating below 5% of GDP by 2013. We also expect that by 2013, France's austerity program, which it is already implementing, will reduce that country's deficit, which never rose to the levels of the U.S. or U.K. during the recent recession, to slightly below the U.K. deficit. Germany, which suffered a recession of similar magnitude to that in the U.K. (but has enjoyed a much stronger recovery), enacted a constitutional limit on fiscal deficits in 2009 and we believe its general government deficit was already at 3% of GDP last year and will likely decrease further. Meanwhile, Canada, the only sovereign of the peer group to suffer no major financial institution failures requiring direct government assistance during the crisis, enjoys by far the lowest net general government debt of the five peers (we estimate it at 34% of GDP this year), largely because of an unbroken string of balanced-or-better general government budgetary outturns from 1997 through 2008. Canada's general government deficit never exceeded 4% of GDP during the recent recession, and we believe it will likely return to less than 0.5% of GDP by 2013. Мне только совершенно непонятна реакция доллара на это известие: вначале резко вниз (это правильно), а затем резко вверх (почему?) Вообще эта новость негативна для доллара по-любому!

|

|

Федрезерв, как частная финансовая корпорация, ведет свой бизнес очень грамотно. Он дает деньги в долг на длительный срок по относительно высокой ставке (в среднем 4% годовых), а берет по очень низкой – меньше, чем за 0,25%. Как ему это удается, вы узнаете из моей статьи: http://mfd.ru/news/articles/view/?id=640 Это дает Федрезерву вполне приличный профит порядка 80 млрд. долларов в год, которые он возвращает Казначейству. При нынешней форме кривой доходности – это очень выгодный бизнес.

Побочный благоприятный эффект этой схемы: Федрезерв является чрезвычайно выгодным и надежным кредитором для американского государства, поскольку он кредитует государство почти по нулевой процентной ставке (немножко отщипывают, пока деньги прогоняются через POMO, лучшие друзья Феда – первичные дилеры, но это несущественно), ведь проценты возвращаются государству. Но, конечно, эта схема будет работать только до тех пор, пока краткосрочная ставка ниже долгосрочной, а ведь бывает и наоборот.

|

|

Сегодня 18.04.11, если цены будут повышаться, то я буду покупать акции ВТБ, ФСК ЕЭС, Сбербанк по 106,61, РусГидро, ЛУКОЙЛ, СевСт-ао и фьючерсы Si-06.11, RTS-06.11, VTBR-06.11, SBRF-06.11, GAZR-06.11, ROSN-06.11, LKOH-06.11. Если цены будут понижаться, то я буду продавать фьючерсы ED-06.11, VTBR-06.11. Торги акциями ГАЗПРОМ, Сургнфгз, Роснефть, ГМКНорНик и фьючерсами GOLD-06.11, Eu-06.11, GMKR-06.11 запрещены из-за экстремальной волатильности инструментов.

|

|

|

|