По замыслу Драги, банки должны были начать кредитовать друг друга, а межбанковские рынок - оживать. Кроме того, предполагалось, что часть организаций решат активно скупать гособлигации проблемных стран, сбивая доходность по ним и облегчая налоговую нагрузку на компании. Вопреки этому большая часть денег потекла обратно в ЕЦБ: финансовые институты принялись наращивать объем срочных депозитов овернайт, учитывая, что средства на них размещаются под символическую доходность в 0,25% годовых. Абсолютный исторический максимум уровень вложений достиг 6 марта нынешнего года, превысив 827,5 млрд евро.

В последующие два-три года будет замедление экономического роста в США, Европе и, вероятно, в остальном мире, поскольку США – это самая крупная экономика. В отношении 2013-2014 годов надо быть очень осторожными. Надо быть особенно осторожным в отношении 2014 года, поскольку именно тогда мы увидим на Западе самую большую неопределенность, большее замедление экономического развития, валюты испытают большие потрясения, будет больше инфляции. Именно на 2014-й придет пик экономической неразберихи, так что проявляйте осторожность, и будьте к этому готовы.

....

Основной риск – это ужасающий рост задолженности на Западе. В Америке многие пенсионные фонды фактически обанкротились. А долг американского правительства? Америка как страна является самым крупным должником в мировой истории.

.....

Единственно, что было бы хорошо для Америки, это резко, сильно сократить бюджет, сократить расходы, сократить налоги и постараться привести свои госфинансы в порядок. Случится ли такое? Нет, конечно же, нет. В Вашингтоне слишком многие круги заинтересованы в том, чтобы тратить деньги других людей.

Граница между восстановлением экономики и возможной рецессией практически стерлась, в первую очередь для таких стран, как США и Великобритания, считает заместитель главного редактора и главный экономический обозреватель газеты Financial Times Мартин Вулф.

В отличие от большинства аналитиков, которые требовали более жесткой экономии средств и ужесточения бюджетной политики, Вулф считает, что бюджетный дефицит – это практически единственный фактор, который удерживает глобальную экономику на плаву.

...

Дело в том, что дефицит бюджета США и Великобритании не провоцирует массового бегства с рынков этих стран. И при этом власти стран на фоне нехватки средств вынуждены прибегнуть к единственному альтернативному методу поддержки экономики в кризисных условиях - методу сохранения низких ставок, которые и привлекают частный капитал и международные инвестиции.

...

Вулф утверждает, что ультранизкие ставки с течением времени способствовали притоку крупных инвестиций в недвижимость, в отличие от притока инвестиций в "безопасные активы" в результате финансового кризиса в Азии. Это, в свою очередь, привело к инвестициям в рисковые активы, обеспеченные недвижимостью, что позволило наблюдать восстановление в этом секторе экономики, который является индикатором общего «самочувствия» экономики страны.

Paul Ryan, the Chairman of the House Budget Committee has put forward the latest update of his "Path To Prosperity" plan. It's a budget for the federal government that includes massive tax cuts and tax simplification, with spending cuts to major government entitlements like Medicare, Medicaid, and Social Security.

Here are the big things: Ryan would redraw personal income taxes into two brackets, 25 percent and 10 percent. The plan doesn't exactly specify yet what income would qualify you for the higher bracket.

There would also be a massive drop in corporate taxes from 35 percent to 25 percent. And there would be hardly any tax deductions either.

There are hundreds of little details that you can find in the plan itself.

The tone for today's U.S. trading session was set overnight during the Australian trading session. At the AJM Global Iron Ore & Steel Forecast conference, BHP Billiton's Ian Ashby warned attendees that China's demand for iron ore was flattening. Rio Tinto also shared that sentiment. The China bears were only emboldened when Chinese policymakers announced they would raise the country's gasoline and diesel prices.

Also announcing quarterly earnings before the bell was Jefferies Group. Although, it is one of the smaller investment banks on Wall Street, it is widely accepted as a harbinger of things to come for the rest of Wall Street's earnings. And to the relief of many, Jefferies announced quarterly results that beat expectations driven growth in investment banking and fixed income. This helped lift the entire U.S. financial sector. Bank of America, Citigroup, Morgan Stanley, and Goldman Sachs were all leaders today.

Weak iron ore demand from China isn't just bad news for BHP Billiton. It could be a sign that China's economy is slowing by more than most think, which would have significant implications for the global economy.

The latest price data out of the UK was somewhat contradictory. The annual headline rate of price gains fell to its lowest level since November 2010 at 3.4% in February, however the monthly rate jumped by 0.6% and both the monthly and annual rate were above expectations. This suggests that the Bank of England can't get complacent about price pressures in the UK as inflation may prove to be stickier than expected.

Президент ФРБ Нью-Йорка Уильям Дадли считает, что сигналы улучшения экономики остаются вялыми, а рисков становится все больше: это растущие цены на сырье, малый объем налоговых сборов и слабый рынок недвижимости.

По мнению экономиста, улучшение показателей было обеспечено увеличением материальных запасов страны и ненормально теплой погодой. На вопрос об увеличении программы выкупа ФРС гособлигаций Дадли ответил, что «окончательного решения еще нет», и таким образом повторил ранее озвученную позицию Комитета по открытым рынкам.

Глава Нью-Йоркского ФРБ также нивелировал достижения на рынке труда, о которых заявляют действующие власти. «Если бы уровень участия рабочей силы не снизился с 66% в 2008 г. до 64% в нынешнем, то безработица все еще была бы выше 10%».

По мнению аналитиков, выступление Дадли было пессимистичным.

Подтверждением этих слов могут служить прогнозы Дадли о росте ВВП в этом квартале. Он заявил, что «если запасы делают большой вклад в рост ВВП, то после такого квартала обычно следуют очень слабые периоды». Напомним, в IV квартале 2011 г. американская экономика выросла на 3%, из которых 1,9% пришлись на запасы.

Zero Hedge повторяет свой старый тезис: чтобы избежать окончания операции «Твист», необходимо, чтобы взгляд на экономические перспективы со стороны Феда значительно ухудшился. Что само по себе подразумевает, что рынки акций должны ответить на это снижением.

As macro data trends deteriorate and Dudley demurs, it is becoming increasingly clear that the risks for the US equity market are skewed to the downside as we head towards the end of Operation Twist (and seasonal factors subside). The Fed's 'upgrade' from modest to moderate growth certainly spooked Gold and Treasuries and saw small caps notably underperform but given historical precedence, if Operation Twist ends without a new program beginning, investors will likely expect a drop in equities (broadly) of 8-10% (which coincides with the QE1 and QE2 ends as well as the 1983, 1994, and 2003 normalizations in policy). Reiterating our recent theme, in order to avoid the end of Operation Twist, the Fed's economic outlook would need to deteriorate - which itself is a scenario likely to result in falling stock prices and just as the cause of a 'crash' in PCE towards the end of QE1 and QE2 was a function of higher inflation, we have the current spike in energy prices to ensure this time is no different.

ZH ожидает, что как в случае QE1 и QE2 причиной для такого ухудшения станут высокие цены на энергоносители – процесс, который мы сейчас как раз и наблюдаем.

Рынок высокодоходных бондов в последние 4-6 недель не разделяет оптимизма рынка акций.

As the S&P 500 reaches new multi-year highs and VIX touches multi-year lows, there is one rather large and risk-appetite-proxying market out there that is not as excited. The high-yield bond market has seen record in-flows dropping off recently and for the last four-to-six weeks high-yield spreads, yields, and bond prices have been very flat as stocks have surged ahead. Despite US earnings yields at near-record highs relative to high-yield bond yields, we see little pick-up in LBO chatter suggesting a notable preference for higher-quality junk credit (and/or lack of belief in sustainability of earnings yields) and the recent 'dramatic' outperformance in investment grade credit is a notable up-in-quality rotation (as well as early spread-compression reaction to Treasury weakness recently) that strongly suggests less risk appetite among real money managers (given how 'cheap' high-yield appears across asset classes). Lastly, the ratio of HY bond prices to VIX is near its extreme once again, something we saw occur before the risk flares of 2010 and 2011 surrounding the end of the Fed's QE sessions.

Президент ФРБ Далласа считает, что финансовая система США хорошо фондирована и не нуждается в дополнительных вливаниях ликвидности.

The U.S. financial system is well funded and needs no further injections of liquidity, a top U.S. central banker said on Monday.

"We have filled the tanks, there is plenty of liquidity. We need no more," Dallas Federal Reserve President Richard Fisher told a round table discussion at a business event in London.

Высказывания другого крупного чиновника Феда тоже не предполагают QE3 в ближайшей перспективе.

(Reuters) - The Federal Reserve has not yet decided on whether to embark on a third round of quantitative easing, or QE3, New York Fed President William Dudley said on Mo nday.

A decision on such large-scale asset purchases would depend on how the economy evolves, and would take into account "costs and benefits," Dudley added.

Overall, we think the basis for another rate cut has diminished in the last few months, thus we are not looking for the RBA to loosen policy this year. Instead, the bank may start a tightening cycle next year. The biggest threat to this stance is a possible deterioration in conditions offshore, especially in Europe and China. Also, we will be closing watching employment data out of Australia for any indication conditions in the labour market are worsening. Whilst we expect the unemployment rate to increase somewhat this year, it may not be enough to force more policy loosening from the bank given the rise will likely be partly the result of structural changes which are out of the RBA's control.

Tim Cook, Apple's CEO, and Peter Oppenheimer, Apple's CFO, will host a Conference Call on Monday, March 19, 2012 at 6:00 a.m. PT to announce the outcome of the Company's discussions concerning its cash balance. Apple will not be providing an update on the current quarter nor will any topics be discussed other than cash.

Быстрый взгляд на то, что сейчас происходит в еврозоне

The biggest issue right now remains the size of the European bailout funds--the European Financial Stability Facility and the European Stability Mechanism. While leaders agreed to move up the implementation of the latter from next year to this summer, Germany has in the past opposed measures to run both funds simultaneously. Recently, German leadership has appeared to have given ground on this issue, it is unlikely to support any measures to increase the availability of bailout funds significantly.

Бывший член управляющего совета ЕЦБ заявил, что европейские лидеры должны немедленно помочь Португалии.

This week, former ECB member Lorenzo Bini-Smaghi said that EU leaders need to allocate funds to support Portugal immediately, since the country is likely not to meet its funding needs of €100 billion by 2016. Bini-Smaghi stressed that this second bailout would need to be talked about immediately so as to avert a liquidity crisis when confidence fades. While yields on its government bonds are no longer over 20%, Portuguese debt is still trading at distressed levels.

...

With Greece's second bailout finally in place, investors are looking ahead to the country's next round of national elections, which will probably topple the technocratic leadership of George Papademos--the country's interim leader since early November. Current finance minister Evangelos Venizelos is expected to tender his resignation Monday to start gearing up for the elections as PASOK's candidate.

On a brighter note, this week both the IMF and the European Commission agreed to pay out the funds Greece has been awarded as part of its second bailout. Greek newspaper Kathimerini reports that the first $7.8 billion of those funds will be paid out Monday.

Пример Греции заставит Ирландию добиваться улучшения условий оказания помощи.

Regarded as the strongest of the bailed out economies in the eurozone, Ireland still awaits a referendum on the "fiscal compact" that EU leaders agreed on back in December. The fact that Greece no longer has to pay back completely the debts it owed the ECB have led Irish leaders to continue pushing for better terms to their own bailout deal--lower interest rates with longer maturities on current loans.

Negotiations with EU leaders on this point are still ongoing, but doubts are beginning to mount about whether Ireland will be able to successfully change the terms of their loans this month.

Испания с ее бюджетными проблемами снова в центре внимания.

Spain is once again in the hot seat compared with Italy, with yields on 10 year bonds rising back above those of its counterpart and above 5%. Its public debt hit a new high at 68.5% of GDP, according to WSJ, and EU finance ministers agreed with Spanish Prime Minister Mariano Rajoy that Spain would not be able to meet its budget deficit goal for the year, raising expectations for that from 4.4% to 5.8%.

Meanwhile, the country is seeing little recovery from a housing bubble and high unemployment. On Thursday, Spain's statistics agency announced that home prices had fallen at an annual rate of 11.2% in the last year and 9.6% in the quarter.

При каких условиях опять пойдет приток средств во взаимные фонды?

The persistent negative investment flows at U.S. listed mutual funds specializing in domestic stocks is one of the most important long-term trends catalyzed by the Financial Crisis. AUM has dropped by $473 billion since January 2007 despite the S&P 500 Index’s essentially flat performance over this period. The news is no better since the beginning of 2012 – despite the ongoing rally in domestic equities – with $6.8 billion of further outflows year to date.

Италия имеет большие позиции на рынке деривативов. Зачем?

What was Italy doing with these swaps in the first place? If they were pure and simple interest rate swaps, why didn’t they just issue floating rate bonds in the first place? That is an easier way for them to manage that exposure. More likely the trades were funky and either involved some games with maturities or optionality, that gave them short term benefits but with increased longer term risk. This should be fully disclosed, and more importantly, the mark to market changes should hit the budget in the year the mark to market changes occur. Everyone seems to be acting surprised by the size of the Italian’s derivative book and the fact that it is massively underwater – why? The book is big because they can do trades that hide losses from the annual budget. Investors should demand to know all the derivative trades sovereigns have on and how they are accounted for.

Главный стратег по рынку акций BlackRock ожидает 1550 пунктов по индексу S&P500 в этом году

"We're not changing our target. We could see 1550, and our target will still be accurate. I

Относительно влияния доходности US Treasuries на рынок акций

For me, it's about the pace of increase rather than the level. If we go up 10 basis points per day, as we did early this week, I'm going to get scared fast, but if it's slow but steady as I'm expecting, not a problem at all. Stocks are still cheap relative to bonds."

"In a zero interest rate environment, at the short-end, 2 percent for a 10-year Treasury and very little inflation, 14 times growth for the S&P is cheap."

"We're up 30% since the low of October 1st- for six months, that seems pretty quick for me. I think some people are just praying for a pull-back so they can put some money in."

Относительно QE3

"I don't think we're going to get QE3 if the U.S. economy is growing anywhere close to 3% and unemployment is falling. That's hardly the condition for an emergency, and QE3 is for emergencies. We don't have one, so I think it's on the back burner... The Fed's been a little bit more forward about that and markets have hung in there. For the bears among you, we're appreciating at a slower rate. We're a little overbought. We'll get a correction, but a correction could just be time without much change in price."

Настало время покупать страховку от рыночного расстройства.

The market doesn't seem worried by anything, which is why, according to BofA's Ralph Axel, it's time to go long on volatility as a hedge against a tail risk disaster. It's not that a disaster is likely, it's just that this insurance is extraordinarily cheap right now.

Не потому, что рыночное бедствие вероятно, а потому, что страховка очень дешево стоит.

VIX вблизи исторических минимумов.

The VIX, a measure of implied volatility of the S&P 500, is also near historical lows. At 15.8 (as of Wednesday afternoon) it is a point above its low of 14.6 going back to the beginning of 2008. The VIX fell to these levels 3 times since the beginning of 2008: in August (before the crisis of September 2008), in April 2010 (before the first euro sovereign crisis), and in May 2011 (before the US debt limit crisis and second euro crisis; see chart). We do not mean to imply that the VIX is signaling a crisis, but we do mean to point out that options are cheap. And history tells us that if one is interested in hedging tail risks, the best time to buy is not in the midst of a crisis or a strong recovery, but at times like now when the market is lulled into a belief that the future holds neither large upside nor large downside shocks.

Перечисляются последние рыночные истории, когда VIX был на столь низком уровне.

Такая же низкая волатильность наблюдается и на рынке опционов на американские US Treasuries.

He also notes that the same lack of volatility is seen in options on US Treasuries... there's still a general belief that the market isn't going anywhere.

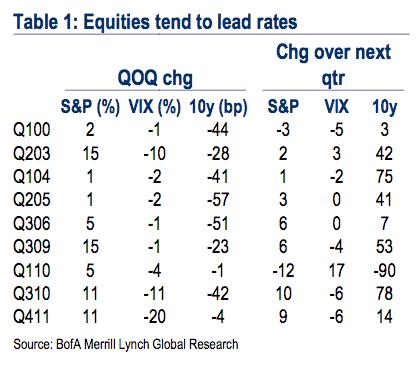

Furthermore, history suggests that a surge in equities (like what we've seen so far in Q1) will be followed by both a rise in yields, and a rise in volatility.

This table shows that going back over the last decade, quarters which saw a rise in stocks tended to see a decline in yields and the VIX, but that in subsequent quarters, 10-year yields tended to jump, and the VIX arrested its fall.

Следующая таблица показывает, что за кварталом рост акций следовал не снижение, а повышение доходности US Treasuries в следующем квартале и VIX препятствовал их падению.

Не очень убедительная закономерность. И какой сейчас считать квартал в этой последовательности – первый или второй?

Так выглядят на одном графике индекс Dow Jones и долгосрочные доходности за столетие

What it finds is that 3 times in the past, a period of sideways stock market action (denoted by the dashed boxes) finally ended when the Treasury market made a turn. In the early 20s, 50s, and 80s, it was a major reversal in yields that caused the market to jut higher. The market's currently in another box, still below its highs of 2007, which of course were right around the highs made in 2000.

Думаю, что в этот раз этого не произойдет, потому что уровень долга Америки таков, что даже доходность 4% по 10-year US T-notes ведет к краху американской экономики.

Gundlach ожидает роста доходности по 10-year US Treasuries в район 3,25, что пагубно скажется на американской экономике

Now that Treasuries have broken out to higher yields after six months of mind-numbingly low volatility, it is logical to expect the move to higher rates to last more than one week," Gundlach said. "The way things look today I think a move toward 3.25 percent would weaken the economy noticeably."

There were two significant shifts in net speculative positioning it the week ending March 13, according to the latest Commitment of Traders report. The first is an acceleration of the short covering in the euro. The second is the extension of short yen positions.

Спекулятивный шорт по EURO уменьшается, а по JPY растет.

There were two significant shifts in net speculative positioning it the week ending March 13, according to the latest Commitment of Traders report. The first is an acceleration of the short covering in the euro. The second is the extension of short yen positions.

The fact that the euro held support near $1.30 is important. That is the bottom of the $1.30 to $1.35 trading range that has confined the euro through most of the first quarter. There is scope for the euro to test the $1.3250-$1.3300 area in the days ahead. The dollar may fare a bit better against the yen, but is more likely to consoldiate then trend higher.

In the week through March 13, the net speculative short euro position was cut from 116.4k contracts to 99.3k. It is the first time the net shorts have few than 100k contracts since early December. The change is almost solely the function of shorts being reduced (16.k) than new longs being established (382).

The net short yen position jumped from 19.4k to 42.4k contracts in the most recent reporting week. This is the largest net short position since April 2011. Since the financial crisis began in the second half of 2007, the net short yen position has been only rarely and briefly larger than it is now. The shift in positioning reflects almost in equal measure longs capitulating (11k) and shorts being established (12k).

Net short sterling edged higher to 41.8k contracts from 37.1k. This is the largest net short position since early December. It was largely a function of new shorts entering the market, but these were in week hands and the fact that $1.56 support held in the spot market suggests that some of these short may have been forced out. Sterling looks poised to re-test the upper end of its range in the $1.59-$1.60 area.

For the most part, Swiss franc, Canadian dollar and Australian dollar positions were little changed. The net short Swiss franc position was cut by about 5k to 14.8k contracts, which is the smallest net short position since in a little more than a month.

The net long Canadian dollar position edged higher by less than 1000 contracts, but it was the sixth consecutive weekly build and the largest since July 2011. Nevertheless, the Canadian dollar appears poised to suffer on the crosses in the days ahead, especially against the euro, sterling and Australian dollars.

The net long Australian dollar position rose to 66.8k from 61.7k, due to an increase in longs and a reduction of short positions are roughly the same amount. The Aussie held key support near $1.04 and can recover toward $1.0650-$1.07 in the period ahead.

И про облигации

Lastly, given the sharp jump in US yields recently, we took a look at the Commitment of Traders for the futures on the 10-year Treasury note.. The net short position leaped to 77.3k from 23.3k and is the largest short position in five months. Longs were cuts by 30.5k and and shorts added about 23.4k contracts.

Противоречия внутри Коммунистической партии Китая, информация о которых практически все время оставалась достаточно закрытой, стали достоянием широкой общественности. ЦК Компартии приняло решение об отстранении от должности одного из самых популярных китайских политиков, члена Политбюро Центрального Комитета КПК, руководителя парторганизации города Чунцин Бо Силая.

"...We know how much money has been flowing into those bonds funds over the last three or four years. All of a sudden they might get a little nervous and say where am i going to go? Where can i get some yield and also some protection against inflation and growth? and that's when I think we're going to see people fleeing the bond market moving into stocks."

Goldman Sachs вешает лапшу на уши клиентам: прогнозирует QE3 уже в апреле

Confused why every asset class is up again today (yes, even gold), despite the pundit interpretation by the media of the FOMC statement that the Fed has halted more easing? Simple - as we said yesterday, there is $3.6 trillion more in QE coming. But while we are too humble to take credit for moving something as idiotic as the market, the fact that just today, none other than Goldman Sachs' Jan Hatzius came out, roughly at the same time as its call to buy Russell 2000, and said that the Fed would announce THE NEW QETM, as soon as next month, and as late as June.

Что нужно делать.

As for Goldman, if one ignores all of the below, the only thing to remember is that Goldman is now selling stocks to, and buying bonds from the muppets.

Вопросы и ответы: с помощью которых GS пытается своих клиентов убедить, что QE3 будет уже возможно на следующем заседании ФОМС в апреле.

Q: What is your current forecast for Fed policy?

A: It has definitely become a closer call, but we still expect another asset purchase program that involves purchases of both mortgage-backed securities and Treasuries. This would expand the Fed's balance sheet, but its impact on the monetary base would likely be "sterilized." We expect this program to be announced in the second quarter, either at the April 24-25 FOMC meeting or the June 19-20 meeting. The argument for April is that this would leave more time before the end of the long-term bond purchases under Operation Twist (more formally known as the Maturity Extension Program), and would thereby reduce the risk of market disruptions as uncertainty about the Fed's role in the market rose. The argument for June is that this would allow Fed officials a bit more time to assess the state of the economy. After June, we believe the hurdle for more action rises, not so much because of the impending presidential election but more because a decision to wait until after the end of Operation Twist would signal greater comfort on the Fed's part with denying the economy additional stimulus.

Peter Tchir of TF Market Advisors про итальянские банки и рынок госдолга

So Italian banks have issued about $100 billion of these ponzi bonds and even in this day, that is a big number.

Banks issue bonds to themselves. Then they get an Italian government guarantee. Then they take those bonds to the ECB and get money, which I assume they use to pay down other debt mostly.

The Italian banks and Italian sovereign debt markets are essentially becoming one and the same. The sovereign has added 100 billion of risk to the banks (that today no one is focused on) and the banks and ECB would have to come up with some new gimmick if the sovereign had problems.

Рынки банковского долга и суверенного долга Италии стали практически одно и то же.

These ponzi bonds ensure that Italian sovereign and bank spreads become 100% correlated over time. The fact that LTRO has daily variation margin adds to the death spiral. The fact that the ECB's outright holdings will be made senior to other holders is also an issue. I have lost track of what the EFSF or ESM are currently doing, or plan to do, but some money is being used up on the latest Greek bailouts, and the reluctance to pre-fund it, means that risk of the market rejecting EFSF or ESM bonds at times of crisis remains high.

Шансы, что рынки откажутся от бондов EFSF и ESM в момент кризиса остаются велики.

PeterTchirofTFMarketAdvisors пишет про различные сегменты рынка бондов

Without a doubt, retail has fallen in love with corporate bonds. Fund flows were originally into mutual funds, and have shifted more and more into the ETF’s. The ETF’s are gaining a greater institutional following as well – their daily trading volumes cannot be ignored, and for the high yield space, many hedgers believe it mimics their portfolio far better than the CDS indices.

The investment grade market looks extremely dangerous right now as the rationale for investing in corporate bonds – spreads are cheap – and the investment vehicles – yield based products.

И про рынок казначейских облигаций

I do not like the move in treasuries. ZIRP can hold down the short end of the curve. Operation Twist can help keep the longer end anchored and focused on the short end, but that is more difficult to accomplish. The further out the curve, the less control the Fed has. With LQD having a very long duration and trading at a premium to NAV, I think there is room for more weakness here. Investors will learn that investment grade bond investments can lose money even as spreads tighten.

В этом месяце наблюдается значительный рост волатильности юаня. Что это означает для экономики и рынков?

This month has brought signals of a subtle regime change in the People‟s Bank of China‟s (PBoC‟s) management of the external value of the Chinese yuan (CNY). We have seen a considerable upturn in the volatility of the daily PBoC fixes for USD-CNY and, more specifically, two sharp fix-to-fix CNY losses.

By and large, that China’s highly manipulated currency market is on the verge of ‘equilibrium’.

That’s to say, the country is no longer attracting enough dollar inflows to justify its long-orchestrated currency manipulation, a.k.a Treasury buying... a.k.a Chinese-led US quantitative easing.

Китай сократил покупку американского госдолга. Кто теперь будет его покупать?

As a result of the shrinking trade surplus and the need to import expensive crude, China does not have the investable dollars it once had. So it is no longer buying US Treasuries at the previous fast pace. At the same time, the US Treasury is issuing debt at the rate of $100B a month. If the Chinese aren’t buying debt, then it must be sold to other dollar holders.

The Australian dollar has long been seen as a China/commodities trade, but Macquarie’s Brian Redican reckons that’s no longer the case. The currency is increasingly influenced by external factors, rather than the country’s own ever-growing mining sector, or its monetary and fiscal policy.

And this, he says, is a momentous shift — so much so that Macquarie now sees the AUD remaining around its current levels for several years, and only gradually sliding to $1.05 by 2015. Their previous forecast was a fall below USD parity by the end of this year.

75% австралийского выпуска бондов находится за рубежом

It’s now reached the point where 75 per cent of national government bond issuance is held offshore. And yields are high against other AAA sovereign bonds: close to 4 per cent for 10-year maturities.

В дополнение темы: речь заместителя главы ЦБ Австралии

Во время Всекитайского собрания народных представителей премьер Госсовета Вэнь Цзябао всенародно объявил о необходимости реформы партийного и государственного руководства. Без этого бессмысленны экономические реформы.

Кризис в китайском руководстве

В ожидании отставки глава китайского правительства подвел итоги своей деятельности и предрек дальнейшее замедление экономики.

Комментируя обменный курс юаня, Цзябао пообещал постепенно расширять коридор его колебаний. Хотя надобности в этом уже почти нет

..."С тех пор как в 2005 году была запущена реформа курсообразования, юань укрепился к доллару на 30%. Можно сказать, что реальный курс юаня достиг сбалансированного уровня," - считает Вэнь Цзябао.

В целом выступление председателя Госсовета КНР выглядит пессимистично. Он много извинялся за ошибки руководства, говорил о неудачах правительства.

China Speech And A Word Of Warning - Chinese Premier Wen Jiabao gave a speech yesterday and the Shanghai stock market got knocked for a loop (down 340 Dow equivalent points). The media feels that was due to his warning about housing. That may be but another part of the speech caught my eye.

Wen warned that major political change is needed lest the nation fall victim to another “cultural revolution”. Was this a slightly veiled reference to the recent actions and statements of that other Chinese leader, Party Leader Bo Xilai? We’ll try to do some research on that as its implications could be enormous. A power struggle in China is clearly not priced into world markets.

Голдман считает, что продажи американских облигаций связаны с последним заявлением ФОМС и призывает продавать 10-year US Treasuries.

Last night’s FOMC statement ‘marked-to-market’ the committee’s assessment of US economic conditions, which continue to gradually improve. Attention now turns to the minutes of yesterday’s policy meeting, which may reveal whether easing options were contemplated after the expiration of ‘Operation Twist’. US Treasuries sold off yesterday, and are now breaking above the yield range in place for many weeks. The 10-year US-Germany differential, now at 40bp, is at the widest level since last November. A wider spread is in line with our valuation metrics. But the level of intermediate yields remains about 25-50bp too low on both sides of the Atlantic. Using 10-year bond futures (TYM2), we would recommend short at 129-17 for a target of 126-00 and tight stops on a close above 131-16.

Аукцион 30-year US bonds: самая высокая ставка доходности с августа 2011г. – через несколько дней после понижения рейтинга США.

As has been noted all this week, starting with Monday's 3 Year auction which printed at the highest yield in 5 months, the $12 billion 30 Year Bond did not surprise, and at a yield of 3.381%, just inside of the When Issued 3.385%, it priced at the highest yield since August 2011, or just days after the US downgrade. The Bid To Cover was 2.70, on top of the TTM average of 2.68. Take downs were a carbon copy of February, coming at 14.7%, 29.0% and 56.3% for Directs, Indirect and, of course, Dealers. Does the yield have a ways to go? Oh yes - back in February 2011 the 30 Year priced at 4.75%, and then the slow steady decline commenced. What happens next? Will the US need another downgrade for yields to paradoxically slide? Or will the Fed truly leave the UST curve untouched by phasing out its market subsidization? Hardly: as a reminder, here is where we stand: $1 trillion in bond issuance in the next 10 months, and $100 billion in bond sales by China in December (with the latest TIC data pending). Forget stocks, and keep your eyes glued to the bond market. Things are starting to get interesting, especially for the Fed whose DV01 of $2Bn means that every basis point rise in yields means less P and more L.

Что-то странное происходит на рынке бондов. Доллар укрепляется – при этом начинается какое-то повальное бегство из трежерей.

Альтернативный взгляд на недавнюю слабость в трежерях

The last few weeks have seen massive, record-breaking amounts of investment grade USD-based corporate bond issuance, at the same time dealer inventories for corporate bonds are at multi-year lows and Treasury holdings at all-time-highs. In general to underwrite the massive corporate bond issuance, dealers will place rate-locks (or short Treasuries/Swaps in various ways) to control the yield and sell the idea of the 'spread' to clients (which is where most real-money buyers will be focused on value. We suggest that the almost unprecedented corporate issuance and therefore need for rate-locks has provided a significant offer for Treasuries that the dealers (who are loaded) and the Fed (who is only minimally involved) was unable to suppress. The key question, going forward, is whether the expectations of a much lower issuance calendar will relieve this marginal offer in Treasuries and allow rates to revert back down?

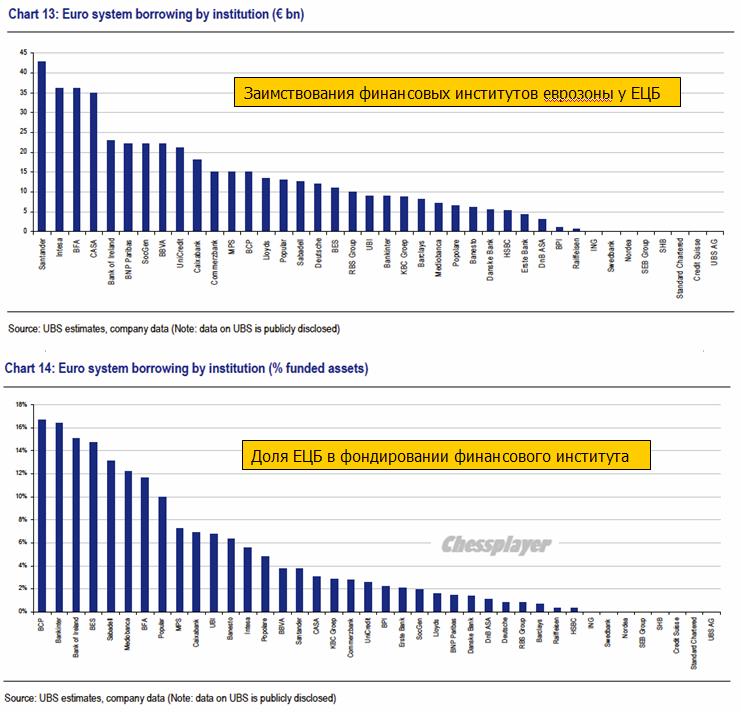

В феврале заимствования испанских банков у ЕЦБ достигли рекорда

As Banco de Espana just released earlier today, Spanish banks have borrowed a record €152 billion in February, a €19 billion increase from January. At least we now know what the capital shortfall was in Spain since pre-LTRO days, when total borrowings were €98 billion

Экс-голдманист критикует нравы, царящие в компании.

How did we get here? The firm changed the way it thought about leadership. Leadership used to be about ideas, setting an example and doing the right thing. Today, if you make enough money for the firm (and are not currently an ax murderer) you will be promoted into a position of influence.

What are three quick ways to become a leader? a) Execute on the firm’s “axes,” which is Goldman-speak for persuading your clients to invest in the stocks or other products that we are trying to get rid of because they are not seen as having a lot of potential profit. b) “Hunt Elephants.” In English: get your clients — some of whom are sophisticated, and some of whom aren’t — to trade whatever will bring the biggest profit to Goldman. Call me old-fashioned, but I don’t like selling my clients a product that is wrong for them. c) Find yourself sitting in a seat where your job is to trade any illiquid, opaque product with a three-letter acronym.

Apple теперь больше, чем весь розничный сектор США

A company whose value is dependent on the continued success of two key products, now has a larger market capitalization (at $542 billion), than the entire US retail sector (as defined by the S&P 500). Little to add here.

Исторический день: цены на бензин достигли рекорда

Presented with little comment except to remind all those newly refreshed consumers that for every penny rise in pump prices, more than $1bn is added to the hoousehold spending bill (assuming driving habits are unaffected - which brings its own set of unintended consequential events). And in the past month alone, gas prices have increased by precisely 30 cents.

Способна ли девальвация йены разрушить глобальный рост?

Seemingly hidden from the mainstream media's attention, we note that the last six weeks has seen the second largest devaluation in the JPY since Sakakibara's days in the mid-90s. As Sean Corrigan (of Diapason Commodities) notes, this has to be putting pressure on Japan's Asian neighbors - not least the engine of the world China. Furthermore, JPY on a trade-weighted basis has cracked through all the major moving averages and sits critically at its post-crisis up-trendline. As we noted last night, perhaps Japan really is toppling over the Keynesian endpoint event horizon. JPY weakness and the carry trade may not be quite as hand in hand if rates start to reflect any behavioral biases, inflation (or more critically hyperinflation) concerns any time soon.

The dollar continued to gain ground against the yen during the session, with the pair rising to its highest level since April 2011. The divergence we expect to see between the BoJ and Fed, as the BoJ continues down the loosening path and the Fed becomes increasingly optimistic, may provide a floor for USD/JPY, thus the path may be clear for a push towards 90.

Не могу с ними согласиться. Считаю, что скорее прав Джон Тейлор.

NEW YORK--(BUSINESS WIRE)--JPMorgan Chase & Co. (NYSE: JPM) today announced the following actions taken by its Board of Directors:

Declared a quarterly dividend of $0.30 per share on the corporation's common stock, an increase of $0.05 per share. The dividend is payable on April 30, 2012 to stockholders of record at the close of business on April 5, 2012

Authorized a new $15 billion equity repurchase program, of which up to $12 billion is approved for 2012 and up to an additional $3 billion is approved through the end of the first quarter of 2013

Дивиденды будут выплачены акционерам, которые окажутся в реестре на закрытие рынка 5 апреля 2012 года.

Из 15 млрд. выкупа акций на 2012 год установлен лимит в 12 млрд,, еще 3 млрд. – в первом квартале будущего года.

Однако:

The timing and exact amount of common stock and warrant purchases will be consistent with the Firm’s capital plan and will depend on various factors, including market conditions, the Firm's capital position, internal capital generation, and organic investment opportunities. The new repurchase program does not include specific price targets, may be executed through open market purchases or privately negotiated transactions, including utilizing Rule 10b5-1 programs, and may be suspended at any time.The equity repurchase program replaces the prior $15 billion program that had approximately $6.05 billion of remaining authorization.

JPMorgan Chase & Co. (NYSE: JPM) is a leading global financial services firm with assets of $2.3 trillion and operations in more than 60 countries. The firm is a leader in investment banking, financial services for consumers, small business and commercial banking, financial transaction processing, asset management and private equity. A component of the Dow Jones Industrial Average, JPMorgan Chase & Co. serves millions of consumers in the United States and many of the world’s most prominent corporate, institutional and government clients under its J.P. Morgan and Chase brands. Information about JPMorgan Chase & Co. is available at www.jpmorganchase.com.

Хочу обратить внимание на следующие моменты в заявлении JPMorgan.

Программа по выкупу акций призвана заменить действующую предыдущую программу с таким же объемом, выполнение которой еще пока не закончено – осталось по ней купить акций на 6,05 млрд. долларов.

Новая программа выкупа может быть приостановлена в любой момент.

По сути никакого нового байбэка нет. Это всего лишь свист – рыночная манипуляция.

Индекс волатильности VIX снизился до 5-тилетних минимумов

VIX at its lowest (sub-14%) since Summer 2007...

and the Volatility term structure, its steepest EVER...

Short-term volatility (risk) is the lowest relative to medium-term risk EVER - is this the biggest ever levered bet on FOMC calmness into European election event risk? Or more technically is this late forced unwinds of legacy long vol/steepeners into the Greece March 20th event risk (which seemed like a decent trade looking for a risk-flare). Given the steepness of the rest of the curve, it certainly feels very technical (flow) driven.

Крупнейший управляющий валютным фондом объясняет, почему падает йена.

Падающая йена – признак крупных проблем, стоящих перед Японией?

Вовсе нет. В недавней записке глава крупнейшего валютного фонда Джон Тейлор объясняет, что двигает йену.

Is the tanking yen -- which we just covered -- a sign of some major problem coming to Japan?

No, not really.

In a recent note, John Taylor of currency hedge fund FX Concepts explains what drives the yen... it's basically risk appetite.

When people want to take more risk, they dump yen. And for the first time in a while, people are feeling good.

That being said, Taylor doesn't expect this to last, and he expects the yen to hit new highs later this year.

Дело вовсе не в каких-то проблемах в самой Японии. На йену давит аппетит к риску.

Когда хотят взять больше риска, то продают йену. И первое время люди в целом чувствуют себя хорошо.

Можно сказать, что Джон Тейлор не ожидает, что это продлится долго и йена в этом году опять достигнет новых максимумов.

Тейлор также объясняет: С момента финансового кризиса 2007 года йена укрепилась сильнее, чем ей следовало бы. Йена сильно коррелирует с бизнесциклом, почти так же как доллар, даже сильнее.

Когда на рынке настает коллапс, управляющие хеджфондов продают активы и покупают йену. От этого она становится сильнее.

Bottom line: At least for now: What drives the yen is the alternation between risk on and risk off, whether Japanese investors are investing abroad, and whether hedge funders are borrowing in yen to buy various assets. When people are investing more and taking risks, that's yen negative.

Самокритика японского министра финансов: он признал, что ситуация с бюджетом в Японии даже хуже, чем в Греции

In a stunning turn of events, a Japanese Ministry of Finance official admits to Richard Koo's worst nightmare "Japan is fiscally worse than Greece". Bloomberg is reporting that, at a conference in Tokyo, Yasushi Kinoshita says Japan's 2011 fiscal deficit was up to 10% of GDP and its debt-to-GDP has soared to over 230%. What is more concerning is the Kyle-Bass- / Hugh-Hendry-recognized concentration risk that Kinoshita admits to also - with a large amount of JGBs held domestically, the Japanese financial system is much more vulnerable to fiscal shocks (cough energy price cough) than Europe.

Danske Bank про сегодняшнее заседание Банка Японии

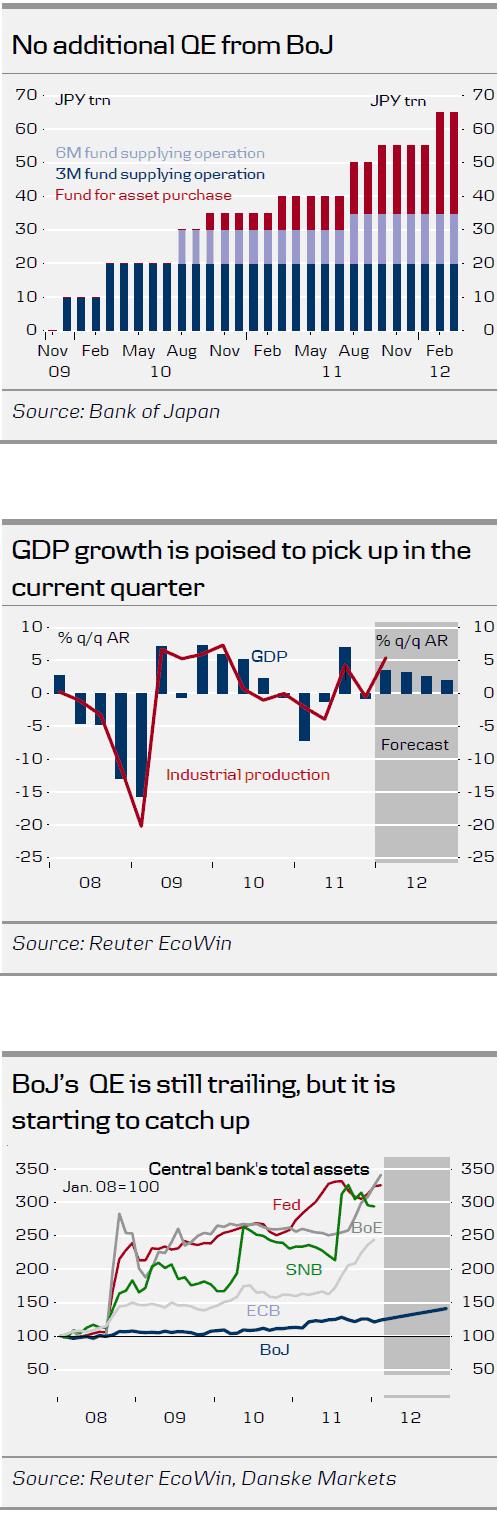

The Bank of Japan (BoJ) as expected left its leading interest rate and the size of its quantitative easing programme unchanged in connection with today's monetary meeting. It did increase the size of funds available in a long-term growth fund by JPY2trn, but this should not be regarded as a major easing move. BoJ's view of the economy was slightly more positive.

With growth rebounding, we do not expect the ceiling for asset purchases to be raised further in H1 12 unless JPY for some reason resumes its appreciation path. However, we do expect the ceiling for asset purchases to be raised further in H2 12 to create space for continued asset purchases in 2013.

Как и ожидалось, Банк Японии (BoJ) оставил ставку и объем программы QE без изменений. Он только увеличил на 2 трлн. долларов размеры фонда по поддержке роста (GSFF).

BoJ announced that it will add JPY2trn to its Growth-Supporting Funding Facility (GSFF) so that total resources in the GSFF are now JPY5.5trn. The purpose of GSFF is to extend loans to projects that support longer-term structural adjustment in the Japanese economy. BoJ does not regard the GSFF as part of the QE programme. In addition, the increase in the EFSF is too small compared with the overall size of the QE programme to make a big difference. Hence, it would be wrong to regard today's increase in GSFF as a major easing move by BoJ.

However, one board member (Miyao) proposed a JPY5trn increase in the asset purchase programme, but the rest of the nine BoJ board members voted against the proposal.

BoJ's view of the economy was slightly more positive. Regarding economic activity, it stated, "...it has remained more or less flat, although it is showing signs of picking up". In the statement from the previous meeting, BoJ just said, "economic activity has been more or less flat".

И оценка будущей монетарной политики BOJ:

With growth improving and growth possible exceeding 3% q/q AR in Q1 12, we do not expect BoJ to raise the ceiling for asset purchases further. The implication of the 1% inflation target introduced at the previous monetary meeting is, in our view, that the ceiling for asset purchases will be raised further at some stage in H2 12 to create space for continued asset purchases in 2013. Should JPY for some reason resume its appreciation path, this would force an earlier and larger expansion of the asset purchases. We think renewed intervention in the FX market in unlikely unless USD/JPY breaks below 75.5.

While BoJ's QE continues to trail other major central banks, it has started to catch up and will probably continue its asset purchases longer than most other major central banks.

Danske Bank не ожидает продолжения QE в первом полугодии, а во втором считает вероятным.

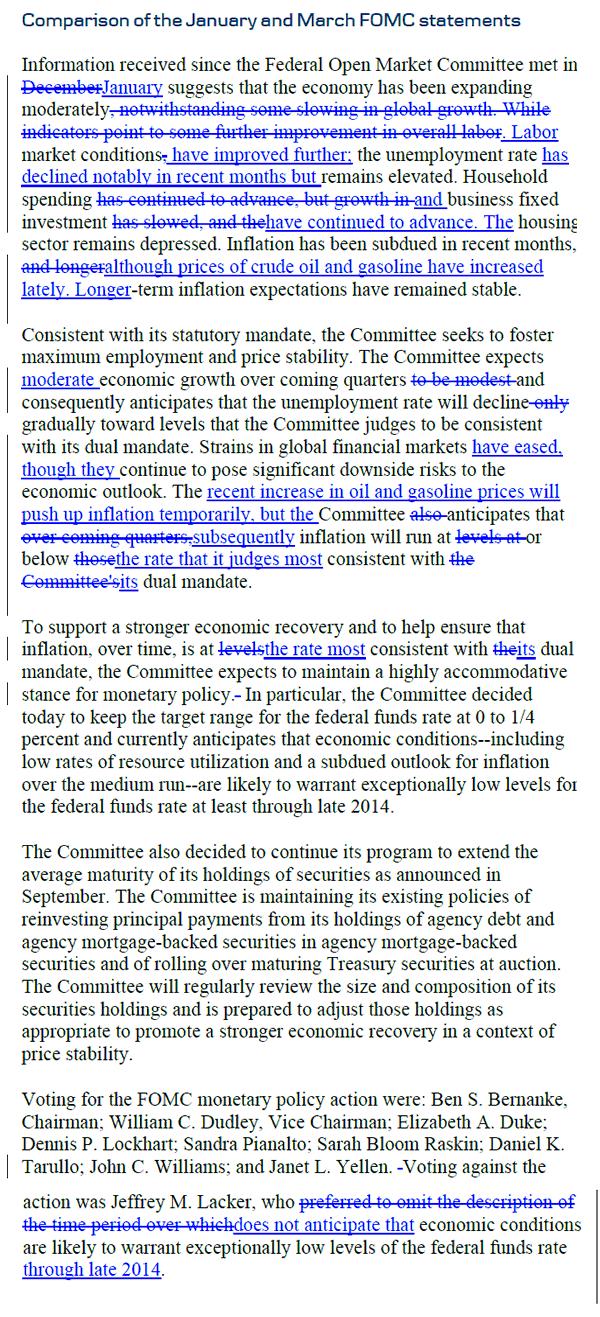

FOMC Meeting: We expect no change, in line with consensus.

BoJ Meeting: The BOJ took the market by surprise at its February MPM by (1) increasing its Asset Purchase Program budget by 10 trillion yen and (2) citing a 1% CPI inflation goal “for the time being”. Political pressure has not abated since the February MPM. At this week's MPM we expect the BOJ to extend its Fund Provisioning to Strengthen the Foundations for Economic Growth, since this is due to expire at the end of March. We also think reference will be made to the pace of upcoming asset purchases.

Вот почему USD/JPY растет! Ждут продолжения интервенций. С трудом верится, что второй месяц подряд.

ECB Draghi Speech

Ecofin Meeting

Ниже идут прогнозы по некоторым экономическим данным. Интересно будет проследить за тем, как они сбудутся.

Wed 14 March

Euro area CPI (Feb): Consensus expects a slight increase to February inflation, 2.7% from 2.6% yoy.

Euro area IP (Jan): Consensus expects further contraction of -0.8%, compared with last month’s -2.0% yoy.

United States CA (Q4): We expect a slight widening of the current account deficit on the back of larger than expected trade deficits in Q4. GS: -$119 bn, consensus expects -$114.2 bn, widening from -$110.3 bn.

Fed’s Benanke SpeechThu 15 March

US Producer Prices (Feb): Producer prices probably received a headline boost in February. GS: +0.37, at 0.5% mom, consensus is up from the previous value +0.1% mom.

US TIC Data (Jan): As always, we will look at the quality of capital inflows into the US. TIC portfolio inflows have recently been geared towards inflows into US treasuries, while US investors tend to be pretty systematic buyers of foreign stocks and bonds. Last +$17.9 bn.

Fri 16 March

US Consumer Prices (Feb): Consumer prices probably received a headline boost in February, while we expect a moderation in core inflation measures. GS: +0.45%, consensus expects 0.4% mom, slightly up from 0.2%.

US IP (Feb): We expect industrial production to benefit from strong gains in vehicle output. GS: +0.6% mom, consensus expects 0.4%, up from 0.0% last month.

The jump in yield from 0.347% to 0.456% may not sound like much, but that is what just happened following the pricing of the latest $32 billion in 3 Year paper, which came at the highest rate since October's 0.544%. And considering that anything under 3 years is virtually risk free courtesy of ZIRP, this move is actually far more pronounced than it appears on the surface.

We do not expect additional QE in the coming months

We do not expect BoJ to announce any additional QE in connection with this week's monetary meeting.

Going forward the most important question will be BoJ's commitment to its new inflation target. The suspicion remains that the easing move on 13 February was mainly driven by external political pressure and less by real conviction by the BoJ board members of the need for a more aggressive monetary stance. For that reason the release of the minutes from the 13 February monetary meeting on 16 March could prove to be more interesting than tomorrow's statement.

With GDP growth poised to rebound in Q1 (possibly above 3% q/q AR), we do not expect BoJ to announce additional QE in the coming months unless JPY for some reason resumes appreciating. The purpose of Japan's FX intervention policy remains solely to stem the appreciation of JPY. Because Japan's intervention policy has been criticized by both the US and the EU, we do not expect to see renewed intervention unless USD/JPY revisits earlier lows below 76. Overall Japan's policy of attempting to “draw a line in the sand” on a stronger JPY has gained credibility. The market increasingly understands that a substantial appreciation will be met by more aggressive monetary easing and possibly even renewed intervention in the FX market.

In our view the ceiling for asset purchases could be raised further in H2 12 to make room for continued asset purchases in 2013.

Danske Bank также не ожидает каких-либо действий от Федрезерва

Following the positive employment report for February, we believe that the FOMC will take a wait-and-see approach at its monetary policy meeting tomorrow. The recent improvement in the labour market does in our view rule out the announcement of new easing measures. However, the door for further easing will be kept open, given Bernanke's wondering over the apparent decoupling of growth and jobs data. Hence, we need more solid economic data before the Fed will make any material changes to its economic projections.

Danske Bank оценивает шансы на новый раунд QE в этом году только в 25%.

We are relatively upbeat on the US economic outlook for the coming six months and we believe that the chance of another round of Fed easing this year is only around 25%.

Banks that found themselves with above 10% of funded assets in public sector money have often either been nationalised or, like Lloyds and Bank of Ireland, have undertaken massive equity issuance in order to change their balance sheet sufficiently to make a full return to the private sector.

It will come as no surprise to any reader that volumes in general are dismal. This leads inevitably to the question of just how liquid markets are in general. This may not be a critical question for mom-and-pop buying some IBM or CAT at the margin but for institutional investors it is critical to the decision to enter a position. Pairing off reward expectations with risk concerns tends to focus too much on volatility and too little on liquidity and by looking at daily market turnover and the bid-offer spread of each asset class, UBS finds taking liquidity into account can make a huge difference to performance (and risk-appetite). Unsurprisingly, the most liquid assets are large cap equities and US Treasuries. The least liquid assets include various fixed income securities, and in particular high yield credit. Perhaps this goes a long way to explaining why US Treasuries have maintained their strength and why large cap equities have been so strong relative to credit markets (a topic we have discussed at length) as money finds its 'easiest' hole to fill and thanks to liquidity concerns, high yield credit investors remain more pragmatic entrants to an ever-inflating bubble of liquidity (as exits will be small and crowded at the first sign of tightening). We suspect the increasing dispersion between the most and least liquid securities in each asset class will likely feed on itself as fewer funds are willing to 'earn' an 'illiquidity' premium given the bigger binary risks facing all markets.

Маленькие валюты крушат большие. Корзина из 20-ти перечисленных ниже валют (G20) превосходит по всем статьям большую четверку (USD, GBP, EURO, JPY)/

The "small" currencies are crushing the bigs.

Specifically, basket consisting of The Aussie dollar, Canadian Dollar, South African Rand, Norwegian Kroner, Swedish Kroner, New Zealand Dollar, Singapore Dollar, Taiwanese Dollar, Colombian Peso, Indian Rupee, Indonesian Rupiah, Russian Ruble, Turkish Lira, Argentine Peso, Brazilian Real, Mexican Peso, Chinese Yuan, and the Malaysian Ringgit has clobbered a basket of the bigs: The Dollar, the British Pound, the Euro, and the yen.

Главный экономист Дэвид Костин по рынку акций GS видит S&P500 на 1250 пунктах к концу году.

The S&P 500 closed at about 1,370 at the end of last week, exceeding David Kostin's target of 1,250 for the end of 2012. Kostin, chief U.S. equity strategist at Goldman Sachs, told Bloomberg TV that he is sticking by his forecast despite the S&P's recent run.

Костин называет три причины:

Kostin said there were three main reasons for his call:

The U.S. economy is stagnating, growing below trend.

In a weak economic growth environment, markets historically have a flat multiple

2012 is expected to see earnings growth of only 3 percent.

Вопрос в том, не окажется ли S&P500 сперва на 1500, а потом уже на 1250 ?

Так или иначе косвенно такой прогноз свидетельствует о том, что Костин не ожидает QE3 до конца года?!

Выборы во Франции и Греции могут изменить расстановку сил таким образом, что вопрос о Греции опять встанет ребром.

Put another way, German leaders, particularly Merkel and Schäuble see the writing on the political wall: that both Greece and France are likely going to find themselves with new leadership that is pro-socialism, anti-austerity measures, and most certainly anti-taking orders from Germany.

Германия между тем продолжает подготовку к плану «B»: неконтролируемому и полномасштабному дефолту.

Germany is aware of this, as well as the fact that there is no way German voters will go for bailouts of any more of the PIIGS (even if Germany, the IMF, and ECB had the funds to bail out Spain or Italy... which they don’t). This is why Germany has decided to play hardball with Greece. It’s also why Germany has put into place a contingency plan that would permit it to leave the Euro if it had to.

Германия создала свой национальный стабилизационный фонд: SoFFin.

What is Germany’s “Plan B”? Leave the Euro but remain in the EU (maybe).

If you don’t believe me, consider that in the last six months Germany has:

Passed legislation that would permit Germany to leave the Euro but remain a part of the EU

Reinstated its Special Financial Market Stabilization Funds, (or SoFFin for short)

It is the second of these items (the reinstatement of the SoFFIN) that the western media and 99% of investors have missed entirely. In short, Germany has given the SoFFIN:

€400 billion to be used as guarantees for German banks.

€80 billion to be used for the recapitalization of German banks

Legislation that would permit German banks to dump their euro-zone government bonds if needed.

That is correct. Any German bank, if it so chooses, will have the option to dump its EU sovereign bonds into the SoFFIN during a Crisis.

In simple terms, Germany has put a €480 billion firewall around its banks. It can literally pull out of the Euro any time it wants to. The question is whether its current EU power grab is successful. If it isn’t... and other EU nations refuse to play ball (like Spain has started to) then Germany could very easily leave the Euro.

This is the black swan no one is talking about. If Germany bails on the Euro, the EU will collapse. It will be Lehman Brothers times 10 if not worse.

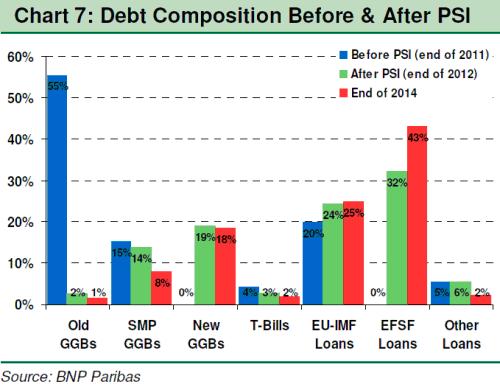

Хотя в целом аналитики позитивно оценивают результаты PSI, говорить о полном решении греческих вопросов пока рано. На протяжении последних двух лет Греция перебивается от одного крайнего срока до другого, едва успевая укладываться в поставленные сроки по оплате долгов, принятию законов и другим обязательствам.

На этом фоне специалисты призывают не торопить события и дождаться больших подробностей программы PSI. "Нам нужно дождаться дополнительных деталей до того момента, как мы будем спокойны. В конечном счете, несмотря на нынешний успех, впереди Грецию ждут парламентские выборы, последствия которых станут новым фактором риска", - комментируют ситуацию в корпорации Credit Agricole.

...если изучить пересмотренные данные, которые показывают, что экономика США была гораздо в худшем состоянии в январе 2009 г., чем сообщалось в то время. Темпы роста в годовом исчислении во второй половине 2008 г. официально оценивались в -2,2%; тем не менее текущие цифры показывают более резкое и пугающее сокращение на -6,3%. Это основная причина, почему экономическая активность в 2009 и 2010 гг. была намного ниже, чем прогнозировалось, и почему безработица была намного выше.

In either case, here is a summary of what Goldman sees happening next: "After the finalization of the PSI process, only small residual transactional uncertainty remains. The new Greece package ensures low funding costs that under certain assumptions could even be sustainable in the long term. Moreover, the exposure of the Greek private sector to the Greek government declines very substantially... ...while the exposure of the European official sector rises to substantial levels.

Late-April elections will be a risk; but polls suggest a pro-EUR government is the most likely outcome. The new government will be tasked with creating a better growth environment.

Голдман настроен позитивно:

Using our GES score, we observe key areas of structural improvement for Greece’s growth environment... ...among others, the creation of a more business friendly environment, the establishment of conditions for increased openness to trade and a more effective rule of law." We will shortly present a far more realistic, and far less conflicted.

Вердикт «Открытой Европы» по долговому свопу Греции: это пиррова победа, которая сеет зерна политического и экономического кризиса в Европе.

In a just released report from Europe think tank OpenEurope, the conclusion is far less optimistic: "The deal sets the eurozone up for a political row involving Triple-A countries. At the start of this year, 36% of Greece’s debt was held by taxpayer-backed institutions (ECB, IMF, EFSF). By 2015, following the voluntary restructuring and the second bailout, the share could increase to as much as 85%, meaning that Greece’s debt will be overwhelmingly owned by eurozone taxpayers – putting them at risk of large losses under a future default. This deal may have sown the seeds of a major political and economic crisis at the heart of Europe, which in the medium and long term further threatens the stability of the eurozone."

Торговый баланс США наихудший за последние 39 месяцев и самое большое трехмесячное снижение за последние двадцать лет.

While NFP dominated the headlines, the US Trade Balance (deficit) limped out and dropped far more than expected. At a $52.565bn Deficit, this is the worst trade balance since October 2008. Perhaps more shocking is the fact that the 3 month drop (rise in deficit) is the largest ever on record, dropping $9.4bn in that period.

Цифры по инфляции создают надежду на смягчение денежной политики Банком Китая

The official CPI figure came in at 3.2%y/y, down from 4.5%y/y in January and the lowest level since June 2010, reaffirming what we already know; the measures adopted by Beijing last year to control inflation have done their job.

Хотя здесь имел место определенный сезонный эффект, но все-равно эта цифра меньше целевого правительственного уровня.

But what does this mean for policy going forward? Premier Wen made it clear in his Government Work Report Beijing intends to maintain a proactive fiscal policy and prudent monetary policy stance. The premier also lowered the official growth forecast to 7.5% for 2012, adding the government is willing to accept lower growth, and whilst this latest CPI figure is lower than expected it is distorted by seasonal factors which makes it very hard to predict. If we attempt to remove some of the seasonality, we see the combined annual rate for January and February is around 3.9%, just below the governments targeted level of 4%. Beijing is also very wary of a possible resurgence in inflation, especially in food prices. Consequently, once we put these factors together we expect the government will maintain its cautious easing of monetary policy.

Late in the session, retail sales and industrial production figures out of China were also below market expectations at 14.7%y/y and 11.4%y/y, respectively.

И про Австралию

In Australia, as we suspected imports decreased but significantly less than exports, which slid 8% over the month. The result was a decline in the trade balance to -673m from 1709m. Australia’s export sector is being hit hard by moderating commodity prices and soft volumes in coal and iron. We expect the export sector will continue to suffer in the short-term from weak levels of demand from some of Australia’s trading partners in Asia.

Билл Гросс по-прежнему делает ставку на ипотечные облигации. Теперь MBS составляют в его портфеле 52% активов.

Привлеченные кредиты слегка уменьшились – с 87,7 до 78,1 млрд., также как и привлеченные кредиты.

The Fed may be using the WSJ to spread rumors of sterilized QE, but Bill Gross ain't buying. According ot the latest update from the world's largest bond fund, the firm lowered its holdings of cash and synthetic Treasury exposure to 38% of total from 41% (even as AUM increased from $250.5 billion to $251.8 billion), while hiking MBS to 52% of AUM: not the highest relative exposure ever, but at $131 billion in Mortgage Backed Debt, certainly the highest in absolute terms. Margin cash declined slightly from $87.7 to $78.1 billion, but one thing that appears to have increased even more is Gross' conviction that QE 3, or to borrow a recent euphemism, THE NEW QE, is coming and it will be all about mortgage backed debt. Of secondary note is that after extending the effective duration of its holdings to an all time high 7.58 years in October 2011, the fund has rapidly cut duration and was at 5.68 at last check as holding in the 1-3 year bucket saw a substantial jump: indicating the ramp up in short duration MBS paper.

5) One hundred billion euros worth of perceived wealth evaporated. That can not be a good thing for a Eurobanking system already capital short, as it raises leverage (quick back of the envelop calculation) by about 6% across the board. It also will not make the interbank market any more trusting, thus increasing the likelihood of perpetual LTRO. LTRO lll looks to arrive sooner than QE lll.

100 млрд. EURO испарились, европейская банковская система должна это почувствовать. Доверие к межбанку подорвано. Это создает потребность в постоянном LTRO.

LTRO-3 наступит скорее, чем QE3.

7) As Europe now speaks increasingly of greater EU financial integration, Sarkozy's poll numbers will be the victim and a less EU friendly individual will likely win the upcoming election. Since France and Germany fortunately have a long and storied history of being the best of friends, and no one in either country would ever pander to nationalist sentiments, this shouldn't present a problem.

8) Given how much angst was caused by the drawn out Greek affair, the Spanish leader knows he has enormous leverage with EU leadership and he can continue to do what he has been doing with regard to ignoring the deficit targets demanded/suggested by the EU. The EU might well bark at him, but they cannot afford to bite at this time. Muchos gracias, Greece.

In light of today’s EMEA Determinations Committee (the EMEA DC) unanimous decision in respect of the potential Credit Event question relating to The Hellenic Republic (DC Issue 2012030901), the EMEA DC has agreed to publish the following statement:

The EMEA DC resolved that a Restructuring Credit Event has occurred under Section 4.7 of the ISDA 2003 Credit Derivatives Definitions (as amended by the July 2009 Supplement) (the 2003 Definitions) following the exercise by The Hellenic Republic of collective action clauses to amend the terms of Greek law governed bonds issued by The Hellenic Republic (the Affected Bonds) such that the right of all holders of the Affected Bonds to receive payments has been reduced.

The EMEA DC has resolved to hold an auction with respect to the settlement of standard credit default swaps for which The Hellenic Republic is the reference entity. To maximise the range of obligations that market participants may deliver in settlement of any such credit default swaps, the EMEA DC has agreed to run an expedited auction process such that the auction itself will take place on March 19, 2012. In light of this expedited auction process, market participants should submit any obligations that they would like to include on the list of deliverable obligations to ISDA as soon as possible.