|

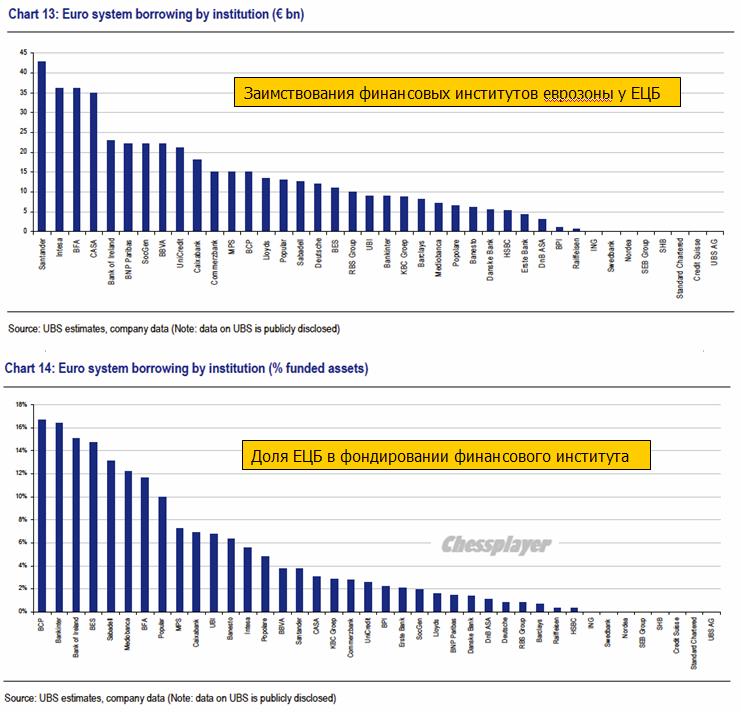

LINKS-ДАЙДЖЕСТ 12 марта 2012 г. Китай продолжит инвестировать в европейские бонды Китай готов помогать и Японии Китай все еще верит в еврозону Банки подсчитали потери из-за Греции Венизелос идет на повышение .................................................................................... теперь англоязычные Summary Of Key Events In The Coming Week События недели от Goldman Sachs Tue 13th March FOMC Meeting: We expect no change, in line with consensus. BoJ Meeting: The BOJ took the market by surprise at its February MPM by (1) increasing its Asset Purchase Program budget by 10 trillion yen and (2) citing a 1% CPI inflation goal “for the time being”. Political pressure has not abated since the February MPM. At this week's MPM we expect the BOJ to extend its Fund Provisioning to Strengthen the Foundations for Economic Growth, since this is due to expire at the end of March. We also think reference will be made to the pace of upcoming asset purchases. Вот почему USD/JPY растет! Ждут продолжения интервенций. С трудом верится, что второй месяц подряд. ECB Draghi Speech Ecofin Meeting Ниже идут прогнозы по некоторым экономическим данным. Интересно будет проследить за тем, как они сбудутся. Wed 14 March Euro area CPI (Feb): Consensus expects a slight increase to February inflation, 2.7% from 2.6% yoy. Euro area IP (Jan): Consensus expects further contraction of -0.8%, compared with last month’s -2.0% yoy. United States CA (Q4): We expect a slight widening of the current account deficit on the back of larger than expected trade deficits in Q4. GS: -$119 bn, consensus expects -$114.2 bn, widening from -$110.3 bn. Fed’s Benanke Speech Thu 15 March US Producer Prices (Feb): Producer prices probably received a headline boost in February. GS: +0.37, at 0.5% mom, consensus is up from the previous value +0.1% mom. US TIC Data (Jan): As always, we will look at the quality of capital inflows into the US. TIC portfolio inflows have recently been geared towards inflows into US treasuries, while US investors tend to be pretty systematic buyers of foreign stocks and bonds. Last +$17.9 bn. Fri 16 March US Consumer Prices (Feb): Consumer prices probably received a headline boost in February, while we expect a moderation in core inflation measures. GS: +0.45%, consensus expects 0.4% mom, slightly up from 0.2%. US IP (Feb): We expect industrial production to benefit from strong gains in vehicle output. GS: +0.6% mom, consensus expects 0.4%, up from 0.0% last month. Market Shorts At 4 Year Lows, In Hibernation For Second Straight Month Шорты на 4-хлетгнем минимуме. В зимней спячке второй месяц подряд. Is Bond Market Whispering Inflation As 3 Year TSY Prices At Highest Yield Since October? The jump in yield from 0.347% to 0.456% may not sound like much, but that is what just happened following the pricing of the latest $32 billion in 3 Year paper, which came at the highest rate since October's 0.544%. And considering that anything under 3 years is virtually risk free courtesy of ZIRP, this move is actually far more pronounced than it appears on the surface. Bank of Japan Preview: No Need for a Surprise This Time Danske Bank о завтрашнем заседании Банка Японии We do not expect additional QE in the coming months We do not expect BoJ to announce any additional QE in connection with this week's monetary meeting. Going forward the most important question will be BoJ's commitment to its new inflation target. The suspicion remains that the easing move on 13 February was mainly driven by external political pressure and less by real conviction by the BoJ board members of the need for a more aggressive monetary stance. For that reason the release of the minutes from the 13 February monetary meeting on 16 March could prove to be more interesting than tomorrow's statement. With GDP growth poised to rebound in Q1 (possibly above 3% q/q AR), we do not expect BoJ to announce additional QE in the coming months unless JPY for some reason resumes appreciating. The purpose of Japan's FX intervention policy remains solely to stem the appreciation of JPY. Because Japan's intervention policy has been criticized by both the US and the EU, we do not expect to see renewed intervention unless USD/JPY revisits earlier lows below 76. Overall Japan's policy of attempting to “draw a line in the sand” on a stronger JPY has gained credibility. The market increasingly understands that a substantial appreciation will be met by more aggressive monetary easing and possibly even renewed intervention in the FX market. In our view the ceiling for asset purchases could be raised further in H2 12 to make room for continued asset purchases in 2013. FOMC Preview: Better Jobs Data Not Enough to Turn the Fed Danske Bank также не ожидает каких-либо действий от Федрезерва Following the positive employment report for February, we believe that the FOMC will take a wait-and-see approach at its monetary policy meeting tomorrow. The recent improvement in the labour market does in our view rule out the announcement of new easing measures. However, the door for further easing will be kept open, given Bernanke's wondering over the apparent decoupling of growth and jobs data. Hence, we need more solid economic data before the Fed will make any material changes to its economic projections. Danske Bank оценивает шансы на новый раунд QE в этом году только в 25%. We are relatively upbeat on the US economic outlook for the coming six months and we believe that the chance of another round of Fed easing this year is only around 25%. LTRO names n’ numbers, revisited Кто и сколько брал денег у ЕЦБ

Banks that found themselves with above 10% of funded assets in public sector money have often either been nationalised or, like Lloyds and Bank of Ireland, have undertaken massive equity issuance in order to change their balance sheet sufficiently to make a full return to the private sector. As US Rakes Largest Monthly Deficit In History, 2012 Tax Revenues Net Of Refunds Trail 2011 How Many Days Will It Take To Sell $10 Million Of... О рыночной ликвидности It will come as no surprise to any reader that volumes in general are dismal. This leads inevitably to the question of just how liquid markets are in general. This may not be a critical question for mom-and-pop buying some IBM or CAT at the margin but for institutional investors it is critical to the decision to enter a position. Pairing off reward expectations with risk concerns tends to focus too much on volatility and too little on liquidity and by looking at daily market turnover and the bid-offer spread of each asset class, UBS finds taking liquidity into account can make a huge difference to performance (and risk-appetite). Unsurprisingly, the most liquid assets are large cap equities and US Treasuries. The least liquid assets include various fixed income securities, and in particular high yield credit. Perhaps this goes a long way to explaining why US Treasuries have maintained their strength and why large cap equities have been so strong relative to credit markets (a topic we have discussed at length) as money finds its 'easiest' hole to fill and thanks to liquidity concerns, high yield credit investors remain more pragmatic entrants to an ever-inflating bubble of liquidity (as exits will be small and crowded at the first sign of tightening). We suspect the increasing dispersion between the most and least liquid securities in each asset class will likely feed on itself as fewer funds are willing to 'earn' an 'illiquidity' premium given the bigger binary risks facing all markets. Daily FX Trading Activity: $4.7 Trillion Дневной объем торгов на Форексе составляет 4,7 трлн. Долларов OIL, CHINA, LIES, BIKE LANES: Jim Rogers Tells All To Business Insider Большое интервью легендарного инвестора Джима Роджерса Get Ready To Be Disappointed With 'Sterilized' QE3 Будьте готовы разочароваться в QE3 sterilized Citi On The Really Simple Currency Trade That's Been Doing Awesome All Year Маленькие валюты крушат большие. Корзина из 20-ти перечисленных ниже валют (G20) превосходит по всем статьям большую четверку (USD, GBP, EURO, JPY)/ The "small" currencies are crushing the bigs. Specifically, basket consisting of The Aussie dollar, Canadian Dollar, South African Rand, Norwegian Kroner, Swedish Kroner, New Zealand Dollar, Singapore Dollar, Taiwanese Dollar, Colombian Peso, Indian Rupee, Indonesian Rupiah, Russian Ruble, Turkish Lira, Argentine Peso, Brazilian Real, Mexican Peso, Chinese Yuan, and the Malaysian Ringgit has clobbered a basket of the bigs: The Dollar, the British Pound, the Euro, and the yen. G20 smalls outperform the G4

Разве это не результат печатания денег? Goldman's Top Strategist Gives 3 Reasons Why The S&P 500 Will Fall To 1,250 Главный экономист Дэвид Костин по рынку акций GS видит S&P500 на 1250 пунктах к концу году. The S&P 500 closed at about 1,370 at the end of last week, exceeding David Kostin's target of 1,250 for the end of 2012. Kostin, chief U.S. equity strategist at Goldman Sachs, told Bloomberg TV that he is sticking by his forecast despite the S&P's recent run. Костин называет три причины: Kostin said there were three main reasons for his call: - The U.S. economy is stagnating, growing below trend.

- In a weak economic growth environment, markets historically have a flat multiple

- 2012 is expected to see earnings growth of only 3 percent.

Вопрос в том, не окажется ли S&P500 сперва на 1500, а потом уже на 1250 ? Так или иначе косвенно такой прогноз свидетельствует о том, что Костин не ожидает QE3 до конца года?! EVANS-PRITCHARD: Global Money Supply Growth Has Peaked--Which Means We're Screwed Глобальное денежное обращение достигло пика... The brilliant-if-generally-gloomy Ambrose Evans-Pritchard of The Telegraph argues that a falloff in the growth rate of the global money supply means that we're headed for an economic slowdown. The Likely Next French President Reveals Why He Wants To Renegotiate Europe's Fiscal Pact Почему вероятный новый президент Франции желает пересмотреть бюджетный договор. JIM O'NEILL: Don't Worry About Friday's 'Not Quite So Good' US Trade Report Джим О’Нейл: Не волнуйтесь. Последний отчет NFP вовсе не так хорош.

|