ISDA Determinations Committee Accepts Question Related to a Potential Hellenic Republic Credit Event

LONDON, February 28, 2012 – The International Swaps and Derivatives Association, Inc. (ISDA), as secretary to the Determinations Committees (the DCs), today announced that a question relating to a potential credit event with respect to the Hellenic Republic has been submitted to, and subsequently accepted for consideration by, the EMEA Determinations Committee.

Заседание ISDA состоится 1 марта в 15.00 мск

In accordance with the Determinations Committee Rules, a meeting will be held at 11AM GMT on Thursday, March 1 to determine whether a credit event has occurred.

Further information regarding the question is available at www.isda.org/credit.

Поддерживать Грецию Германии становится все труднее

Chancellor Merkel failed to get her Chancellor Majority (310 votes in 620 member chamber) but did secure the passing of the EFSF with 305 votes.

Commentators are now busy talking about how she is increasingly finding it hard to negotiate with the Parliament and deal with overall German public opinion. There are several reasons for this:

She and her government told Parliament last year that Germany would be on the hook for a maximum EUR 211 billion. Now fast forward to today and the IMF is insisting that that EU increase the fire-power of bailout mechanisms to 700-750 bln. EUR.

This would mean the German contribution will rise to above 300 bln. EUR - in itself a problem politically (as she promised 211 was the absolute max) but add to this that the German Constitutional Court has already told the Parliament that any support for bailouts in excess of the current German budget (306 bln. in 2012) is risky and destablising. Get the picture? Indeed, the EU Summit this week will be interesting. It seems to me that Merkel will be forced to dig-in her heels on this issue and this will consequently risk the PSI deal and Greece in the process. The stakes are clearly rising.

Citigroup's Buiter put it very elegantly in his Global economic View (27. February 2012 - Why does the ECB not put its mouth where its money is? The ECB as lender of last resort for Euro area sovereign and banks):

'EU policy makers prefer support to fiscally weak Euro Area sovereigns under attack by markets to be provided through the ECB, since that support is off-budget and off-balance sheet, unlike the contributions to the EFSF, ESM'.

This is the key political driver! There is no budget, no balance sheet impact from having Draghi pretend he is the great saviour of everything European (read: banks) but if the ESM, EFSF should need additional capital, then there will need to be a vote - heaven forbid!

The divergence is in the accountability. The ECB is already violating its mandate and the Treaty but they are not up for vote or even accountability so far, hence they will fold their cards first in this game of poker and have done so, again, again and again.

Через ЕЦБ по ряду причин делать это гораздо сподручнее

S&P downgraded Greece to Selective Default (SD) from ‘CC’. S&P said that the downgrade followed the Greek government's retroactive insertion of collective action clauses (CACs). However, if the debt exchange is completed as expected, S&P will raise Greece’s credit rating to ‘CCC’. (RTRS)

-S&P have said they believe Greece would face imminent outright payment default if an insufficient number of bondholders accept the exchange offer.

The EFSF outlook was changed to negative from developing by S&P; 'AA+' ratings affirmed. (RTRS) S&P concluded that credit enhancements sufficient to offset what they view as the reduced creditworthiness of EFSF guarantors are not likely to be forthcoming. The negative outlook on the long-term rating also mirrors the negative outlooks of France and Austria.

The is to make a decision on Greece CDS triggers by 1700 GMT, Wednesday February 29. (FT Alphaville-More) The ISDA announced that a question relating to the Hellenic Republic has been submitted to the EMEA Determinations Committee. The ISDA will decide whether to accept the question for deliberation or reject it.

The ECB have temporarily suspended the use of Greek debt as collateral, reflecting the Greek debt ratings in the light of the PSI agreements. (Sources)

Standard & Poor’s Managing Director Kraemer has commented that the outlook on the Eurozone remains negative, adding that the ECB’s LTRO is not a substitute for reforms, but it does help in the immediate term. (Sources)

The ECB’s Nowotny has said there is no need for ECB’s key interest rate to move below 1% at the moment, adding that the ECB is concerned about the long-term effects of loans. (Sources)

Очень выборочно:

ЕЦБ приостановил принимать облигации Греции в качестве залога.

Важно: ISDA будет принимать решение по поводу контрактов CDS by 1700 GMT, Wednesday February 29 – в среду в 21.00 по Москве

LONDON, February 27, 2012 – The International Swaps and Derivatives Association, Inc. (ISDA), as secretary to the Determinations Committees (the DCs), today announced that a question relating to the Hellenic Republic has been submitted to the EMEA Determinations Committee.

In accordance with the Determinations Committee process, the EMEA Determinations Committee will decide whether to accept the question for deliberation or reject it and this decision will be made by 5PM GMT on Wednesday, February 29, 2012.

В среду пока лишь будет решаться вопрос, принимать ли этот вопрос к рассмотрению.

Суть вопроса:

Does the announcement of the passage by the Greek parliament of legislation that approves the implementation of an exchange offer and vote providing for collective action clauses (“CACs”) that impose a “haircut amounting to 53.5%” (MINFIN Announcement, 2.21.2012) that “shall bind the entirety of the Bondholders [of eligible instruments]” (First Article, Section 9), constitute a Restructuring Credit Event in accordance with Section 4.7 of the 2003 ISDA Credit Derivatives Definitions (as amended by the 2009 ISDA Credit Derivatives Determinations Committees, Auction Settlement and Restructuring Supplement to the 2003 ISDA Credit Derivatives Definitions, published on July 14, 2009) because (i) the European Central Bank and National Central Banks benefitted from “a change in the ranking in priority of payment” as a result of the Hellenic Republic exclusively offering them the ability to exchange out of their “eligible instruments” prior to the exchange and implementation of the CACs, thereby effectively “causing the Subordination” of all remaining holders of eligible instruments, and (ii) this announcement results directly or indirectly from a deterioration in the creditworthiness or financial condition of the Hellenic Republic?

As for what the final size of the LTRO will be, just ask your hotdog vendor: he has as much guidance as anyone else. Regardless of the size outcome, one thing is certain - the banks that are found to use the ECB's Discount Window should prepare for major stock pain, as the market, devoid of easy targets, focuses on them next as the European stigma trade becomes the hedge fund divergence trade du jour. After all there is a reason why the Fed's Discount Window expansion lasted for all of 3 months, and ended up hurting the participating banks (ahem Dexia) more than any other Fed concoction during the early stages of the Depression.

Дисконтное окно Феда просуществовало всего 3 месяца, поскольку пользование им для банков имело слишком сильные репутационные издержки. Вот и на этот раз, те, кто в полной мере воспользуется предлагаемым ЕЦБ LTRO, рискуют надолго получить черную метку и проблемы на межбанке...

Case Shiller продемонстрировал 8-й подряд месяц снижения цен на дома.

The December Case Shiller came, saw, and shut up all those who keep calling for a home price recovery. The Index printed at 136.71 on expectations of 137.11, with the prior revised to 138.24. The top 20 City composite was down -0.5% on expectations of a 0.35% drop. 18 out of 20 MSAs saw monthly declines in December over November, with just the worst of the worst - Miami and Phoenix - posting a dead cat bounce, rising 0.2% and 0.8% respectively. And granted the data is delayed, but the fact that we have now had 8 consecutive months of home price declines even with mortgage rates persistently at record lows, and the double dip in housing more than obvious, can we finally shut up about a housing bottom? Because as Case Shiller's David Blitzer says: "If anything it looks like we might have reentered a period of decline as we begin 2012.

Двойное дно по рынку недвижимости более, чем очевидно и пока не видно признаков, что рынок начинает выбираться из этого дна.

То, что цифры соответствуют текущей обстановке, уже никого не удивляет.

Начинается переход к режиму QE3 –экономического разочарования, - язвительно замечает Zero Hedge.

После LTRO от ЕЦБ следующая очередь за Федом .

And so the transition to the QE3 "economic disappointment" regime begins. Because after the ECB is done with the LTRO it's over for global QEasing, and the Fed is next. Remember- Bernanke's semiannual testimony to Congress is tomorrow. Whatever will he say....

Headline Durable Goods plunges from +3.2 to -4% on expectations of -1%

More painfully, Durable goods non-defense ex aircraft down a whopping -4.5% on Exp of -1.3%, down from +3.4%.

Visually, this is the lowest Durable Goods number since January 2009

Дефолт Греции можно считать почти состоявшимся. Но никакого волнения не ощущается. До 20 марта мы скорее увидим кредитное событие и срабатывание CAC

So far there are no dramatic consequences of the Greek default. The ECB did say they couldn’t accept it as collateral, but national central banks (including Greece’s somehow solvent NCB) can, so no real change. We will likely get a Credit Event prior to March 20th once CAC’s are used to get the deal fully done. Will the market respond much to that? Probably not, though there is a higher risk of unforeseen consequences from that, than there was from the S&P downgrade. It just strikes us that Europe wasted a year or more, and has created a less stable system than it had before. Tomorrow’s LTRO is definitely interesting. It seems like every outcome is now bullish – big take up is bullish because of the “carry” trade. Low take up is bullish because “banks are okay”. Any weak bank looking to borrow from the LTRO to buy sovereign debt would be insane to buy bonds longer than 3 years and take the roll risk, but on the other hand, the weakest and most insolvent, got there by doing insane things in the first place.

Любой исход завтрашнего LTRO будет позитивен для рынков.

Большой спрос – позитивен из-за кэрритрейда. Маленький спрос – потому-что у банков все ок.

Вчера индекс S&P500 наконец обновил максимумы прошлого года, и теперь максимум этого года стал максимумом с лета 2008 года.

Но это не отменяет того факта, что мы по прежнему находимся в медвежьем рынке.

Торговый диапазон вчера был приличный по нынешним меркам – 17 пунктов.

На фоне положительного закрытия рынка отметим заметно выросший VIX. Если это не однодневный феномен, то предвещает близкую коррекцию.

Странно, что одновременно с ростом рынка акций заметно снизилась доходность US notes. Необходимости в этом вроде как нет! На этой неделе нет размещений US notes.

Возможно, это было связано со вчерашним сильным движением в USD/JPY.

Сразу после обновления максимумов рынок перешел в боковик, в котором пребывал 4 последних часа сессии. На локальных максимумах желающих покупать немного.

Zero Hedge подсчитал, что индекс Dow 22 раза за сессию пересекал туда обратно 13000 пунктов (или только туда?!), но закрылся ниже этого «значимого» уровня.

Голосование в бундестаге по Греции не вызвало проблем. 496 голосами против 90 парламент Германии высказался за оказание помощи Греции. Это был почти запланированный позитив и он, как полагается, вызвал ралли в EURO и рискованных активах.

Сегодня кроме статистики, влияние которой я не берусь оценить, никаких событий не ожидается и рынки будут проторговывать текущие уровни.

В настоящий момент американский фьючерс растет на 0,5%, что создает предпосылки для разворачивания сценария, противоположному вчерашнему: положительное открытие американской сессии с последующим возвращением к нулю или в минус с дальнейшим продолжением завтра в азиатскую и европейскую сессию.

Основные события на этой неделе будут разворачиваться в среду-пятницу.

Завтра предстоит бурный день:, выйдут предварительные данные по ВВП США, данные по инфляции в еврозоне, а примерно в 14.15 выйдут данные по LTRO.

Естественно после сегодняшнего роста завтра рынкам перед объявлением об LTRO немного припасть.

Реакция на объявление об итогах LTRO мне видится совершенно непредсказуемой.

В целом, я не вижу индекс S&P500 на этой неделе на уровнях выше 1380 пунктов.

Сегодня я хочу также поговорить о дальней перспективе и оценить перспективы текущего ралли в S&P500 с необычной точки зрения: используя ATR.

На рисунке под графиком индекса S&P500 помещен график ATR(5) – 5-типериодной скользящей средней от среднего истинного диапазона (ATR). Как мы видим долгосрочным (многомесячным) максимумам по индексу S&P500 всегда предшествует период, когда ATR(5) имеет очень малые значения – порядка 10-12 пунктов. Существенные коррекции возникали после того, как ATR(5) преодолевал значение порядка 17, показанное на графике красной линией.

Это ИМХО свойство современного рынка, когда все определяется ликвидностью.

С точки зрения долгосрочной торговли все события, связанные с Грецией, с рейтингами и т.д. это не более, чем шум. Все определяется денежными потоками «умных денег», которые физически не могут быстро разворачиваться и менять направление. Они не умеют метаться (пока еще не научились).

«Умные деньги» не реагируют на новости-шум, они реагируют только на действительно значимые вещи (ВВП, инфляция, QE2, LTRO, валютные интервенции ). Низкий дневной диапазон ATR – низкая волатильность - означает, что «умные деньги» не торопясь заходят в рынок, либо уже выходят, но опять же этот процесс занимает время.

Поэтому, пока ATR(5) держится в районе 10-12, долгосрочным лонгам еще ничего не угрожает, хотя и потенциала для роста уже нет!

Ведь на самом деле я уверен, что сейчас уже идет раздача лонгов!

Я не беру случаи форсмажора (впрочем подавляющее большинство форсмажоров имеют искусственное происхождение) – в данном случае речь идет об обычных условиях торговли.

Разумеется здесь нужно учитывать и фундаментальные условия.

С чем может быть связана низкая волатильность?

Есть две главных причины.

1.Неопределенность ожиданий рынка. Рынок застывает в ожидании. Объемы торгов падают и соответственно ATR падает.

2.Во время стабильного бычьего тренда, вызываемого не положительными макроэкономическими данными и сантиментом (здесь реакция более эмоциональна - следовательно волатильность больше), а избыточной ликвидностью. Это то, что мы имеем сейчас. "Умные деньги" действуют без спешки и сглаживают излишнюю волатильность.

То же самое справедливо и для недельного графика (представлен на рисунке внизу).

Как мы видим, во время всего продолжительного бычьего рынка, начавшегося весной 2003 года, недельный ATR(5) ,был в диапазоне 17-30 пунктов, в то время как с весны 2007 года средний недельный диапазон стал расти, что вылилось потом в совершенно безумную по волатильности осень 2008 года.

Отметим, что когда дневной ATR(5) приближается к 16, коррекция сразу не наступает, а возникает волатильный боковик – движения вверх практически нет и график движется в бок.

Апсайд вверх ограничен 15-20 пунктами. Вниз тоже не пускают, подбрасывая рынок как мячик вверх. Эту фазу можно назвать «прогонкой на хаях». Это когда умные деньги стараются избавиться от как можно большего объема лонгов в предверии захода вниз.

Эта фаза рынка, в которой мы сейчас находимся. И нас по всей видимости ждет еще в течение нескольких недель боковик в диапазоне 1340-1390 пунктов, прежде чем коррекция (медвежий рынок) возобновится.

Вчера индекс S&P500 наконец обновил максимумы прошлого года, и теперь максимум этого года стал максимумом с лета 2008 года.

Торговый диапазон вчера был приличный по нынешним меркам – 17 пунктов.

Сразу после обновления максимумов рынок перешел в боковик, в котором пребывал 4 последних часа сессии. На локальных максимумах желающих покупать немного.

Странно, что одновременно с ростом рынка акций заметно снизилась доходность US notes.

Голосование в бундестаге по Греции не вызвало проблем. 496 голосами против 90 парламент Германии высказался за оказание помощи Греции. Это вызвало ралли в EURO и рискованных активах.

Сегодня кроме статистики (не такой уж существенной) никаких событий не ожидается и рынки будут проторговывать текущие уровни.

Основные события на этой неделе будут разворачиваться в среду-пятницу.

Завтра предстоит бурный день:, выйдут предварительные данные по ВВП США, данные по инфляции в еврозоне, а примерно в 14.15 выйдут данные по LTRO.

Реакция на объявление об итогах LTRO - главное событие последних недель -мне видится совершенно непредсказуемой.

В целом, я не вижу индекс S&P500 на этой неделе на уровнях выше 1380 пунктов.

Опять от 1353 амеры выкупились, да еще с проколом 1370 по фсипу. Не рынок, а тарзанка какая-то, только пуляют снизу вверх. В ноябре-декабре носились вверх-вниз по нескольку процентов в день, вдруг после нового года рынок вообще перестал откатывать, торгуется в линию, пока не приходит слон и не выдергивает фсип к следующему уровню. Небольшие откаты были от 1300, 1330, 1350, 1370. Вроде бы откаты были там, где и должны, но при этом ползучий рост продолжается, и это вытягивает все рынки за волосы из болота. Дакс вчера был -1.7% в моменте, из-за непадающих амеров закрылся около нуля. Запоздалый подъем произошел-таки у япов и у наших под конец месяца. Зачем амеров так держат, да еще совершенно не рыночным образом? До даты, события или уровня? В любом случае начало марта начнется с движения сверху вниз, поэтому очень странно наблюдать, как амеры пытаются закрыть февраль на хаях при полном бездействии продавцов.

Наши вчера консолидировались вокруг 1590 по мамбе. Немного откатила нефтянка, ГП от 196 сразу же откатил на -4 рубля, отдыхали суры после пятничных +7%, а вот сбер продолжали подтягивать к отметке 100, чтобы взять ее сегодня гэпом. Игру на понижение аннулировали в пятницу, а новую не начинают, в то же время демонстрируя отсутствие денег на рынке для мощных покупок. Так что торгуем старые планы, 1620 - мощное сопротивление))).

Все, что смогли показать американские фондовые индексы в понедельник – это закрытие утренних гэпов. Пока не будут известны результаты запуска ликвидности в ходе LTRO-2, инвесторы не станут увеличивать торговую активность на фондовых биржах. Неслучайно, за последнюю неделю совокупные торговые обороты на NYSE, ASE и Nasdaq остаются на минимальных годовых уровнях. Примечательно, что одновременно с подъемом котировок на акции, растут цены и на такие защитные инструменты, как USTreasuries(доходность 10-леток вчера упала до 1,92%). По сути ликвидности так много, что она заперта в ловушке под нулевые процентные ставки при полном отсутствии доходностей по гособлигациям с высокими кредитными рейтингами.

Позиции единой европейской валюты (EUR/USD 1,3430) не сильно ослабили новости о том, что рейтинговое агентство Standard & Poor's ухудшило прогноз по долгосрочному рейтингу EFSF, а также понизило суверенный кредитный рейтинг Греции на две ступени до уровня «селективный дефолт» (SD) в связи с запуском программы добровольного списания долгов. Однако, если инвесторы согласятся с условиями предложенного обмена, рейтинг страны могут вернуть на уровень «ССС». Официально Греция запустит процедуру облигационного свопа в пятницу.

Цены на нефть марки Brentхоть и отошли сейчас от своих годовых максимумов почти на $2, все равно остаются на слишком высоких уровнях, для того, чтобы вызвать распродажу акций нефтяных компаний. Причину просадки котировок «черного золота» стоит искать в заявлении Саудовской Аравии, которая на днях резко увеличила экспорт своей нефти, дабы покрыть нехватку сырья на рынках со стороны Ирана.

Во вторник мы ожидаем увидеть открытие торгов на наших биржах в умеренно-позитивной зоне. Ближайшим сопротивлением по индексу ММВБ является уровень вчерашнего максимума на отметке 1607 п. Не думаю, что мы пойдем куда-то существенно выше с учетом невнятной ситуации на биржах Бразилии и Китая. Думаю сегодня наши индексы стабильно торговаться возле текущих уровней, отчасти копируя настроения на валютных и сырьевых рынках.

По мере приближения к президентским выборам вероятность коррекции на российском рынке акций повышается. Думаю, любой результат выборов не устроит несистемную оппозицию. На улицах усилятся массовые акции протеста, из-за чего наши индексы немного съедут вниз. Публикуемый на этой неделе китайский PMI – тоже источник риска.

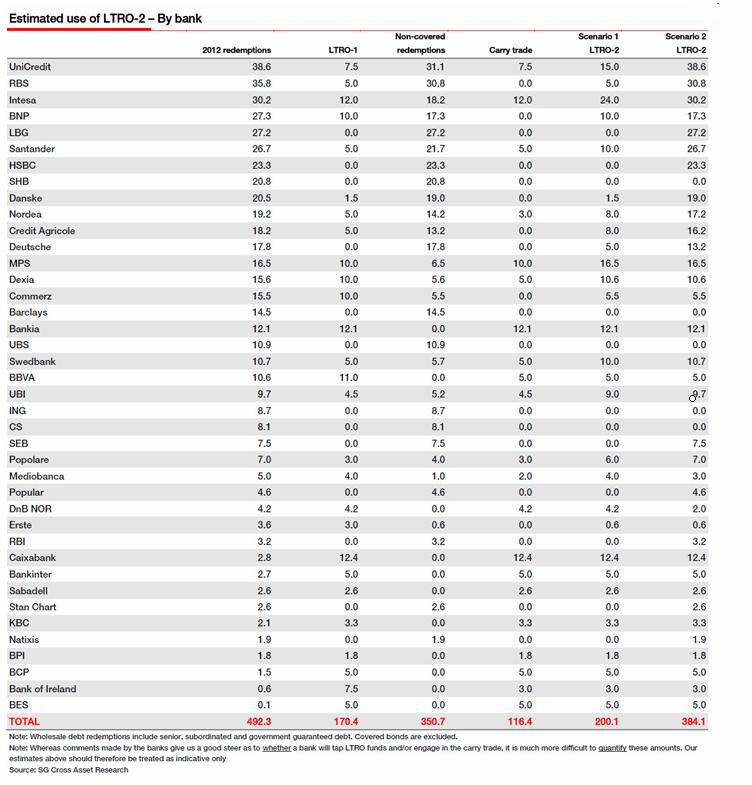

SocGen provides a comprehensive top-down analysis of the drivers of LTRO demand, the likely uses of those funds, and estimates how much of this will be used to finance the carry trade (placebo or no placebo). Italian (25%) and Spanish (20%) banks are unsurprisingly at the forefront in their take-up of ECB liquidity (likely undertaking the M.A.D. reach-around carry trade ) and have been since long before the first LTRO. On the other side, German banks have dramatically reduced their collective share of ECB liquidity from 30% to only 6%. SocGen skews their detailed forecast to EUR300-400bn, disappointing relative to the near EUR500bn consensus - and so likely modestly bad news for risk assets. Furthermore, they expect around EUR116bn of this to be used for carry trade 'revenue' production which will however lead to only a 0.6% improvement in sectoral equity levels (though some banks will benefit more than others), as they discuss the misunderstanding of LTRO-to-ECB-deposit facility rotation. We, however, remind readers that collateralized (and self-subordinating) debt is not a substitute for capital and if the ECB adamantly defines this as the last enhanced LTRO (until the next one of course) then European banks face an uphill battle without that crutch - whether or not they even have collateral to post. Its further important to note that LTRO 2 cannot be wholly disentangled from the March 1-2 EU Summit event risk and we fear expectations, priced into markets, are a little excessive.

[ZH: What we do note is that this is unlikely to be a Goldilocks moment. Too small an uptake, as SocGen expects will lead to risk-off and disappoint markets. Too large an uptake, in our view, will also shock the market - the greater stigma and rising subordination of assets via collateralization will hurt senior unsecured credit and implicitly cost of funding medium-term (shutting private funding channels and increasing public funding dependencies) - leading to risk off. Unless we see EUR475-EUR525bn - just right - then we suspect we will see risk-off either way.]

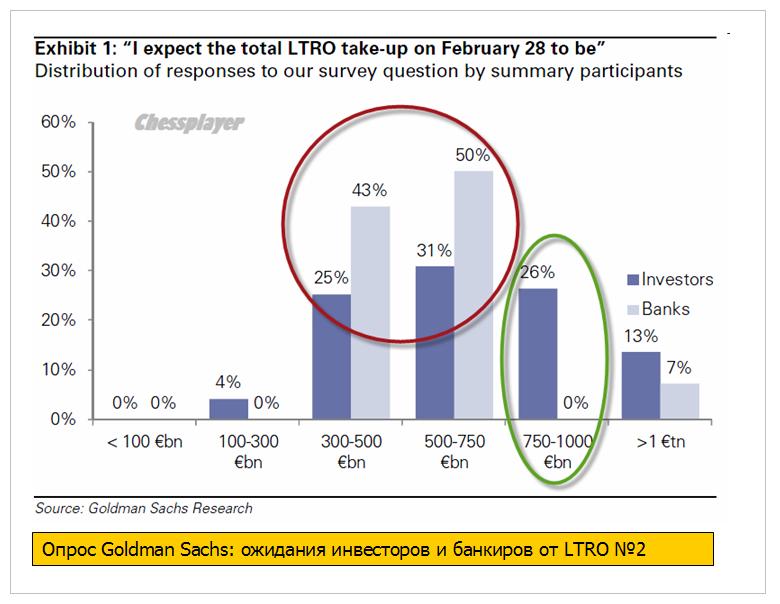

Gaming out the impact of this week's LTRO2 demand on global risk assets is complicated by the ability of banks to mobilize collateral (how much can they pledge to the ECB and how much of that will be 'optimal' given the implicit subordination of senior unsecured debt holders), the use of those funds (carry trade economics are considerably lower and refinancing needs remain high), and the market's expectations (just how much more back-door QE is priced into European - and for that matter - US asset prices). Goldman Sachs surveyed its clients and found a gaping divide between banks and investors with the latter expecting considerably more than the banks - it seems someone will be disappointed - investors hope for more and banks expect to do less.

Ожидания банкиров и инвесторов относительно размера предстоящего LTRO №»2 разительно отличаются. Банкиры ждут гораздо меньшего: по-видимому они гораздо лучше осведомлены о способности банков предоставить подходящий залог.

Банк Англии может еще расширить программу выкупа активов, размер которой сейчас составляет 325 млрд фунтов, заявил председатель комитета по монетарной политике Пол Фишер.

"В этом вопросе необходимо сохранять не зашоренный взгляд на вещи, что мы и делаем. Скорее всего, мы подождем до мая, когда мы подготовим новый экономический прогноз, и, основываясь на нем, примем соответствующее решение. Мы можем в будущем столкнуться с любыми сюрпризами, как положительными, так и с негативными", - заявил он в интервью телеканалу Sky News.

Двадцатка министров финансов отказалась увеличивать фонды МВФ.

And below are some of the key excerpts from the G-20 communique (source)

We are reviewing options, as requested by leaders, to ensure resources for the IMF could be mobilized in a timely manner. We reaffirmed our commitment that the IMF should remain a quota-based institution and agreed that a feasible way to increase IMF resources in the short-run is through bilateral borrowing and note purchase agreements with a broad range of IMF members. These resources will be available for the whole membership of the IMF, and not earmarked for any particular region. Adequate risk mitigation features and conditionality would apply, as approved by the IMF Board. Progress on this strategy will be reviewed at the next ministerial meeting in April. Other options mentioned by leaders in Cannes such as SDRs are under review."

Автор статьи Peter Tchir сравнивает последние меры по лечению европейского долгового кризиса с таблетками с эффектом плацебо.

Пациенту временно становится лучше, но эффект очень кратковременен и реального лечения болезни нет.

Making it even more difficult to determine if a policy is working is the “placebo” effect. The market is being fed a lot of medicine (pun intended). LTRO and Greek “resolution” being the latest medicines. But are these treatments really working or are we rallying on a diet of pablum?

The LTRO was designed to support the market, the market is up, so the LTRO must be working. That at least is the logic many investors are applying. They see the improvement in sovereign debt yields, the avalanche of “positive” (if unfounded) headlines, and the relentless march higher of the stock market. So the plan is working? Not so fast. The treatment was designed to help the stock market. The stock market is encouraged by that and believes it is getting better. That price action in turn convinces more people that things are better or fixed, and creates further demand for stocks. But is it real or are we just in another “Placebo Effect” stock market rally? The problem with the patients who get better on the placebo, is that the effect tends to be short-lived since nothing is actually fixed.

Рынки недвижимости и розничной торговли, получившие наибольшие выгоды от кредитного разгула ждут очень тяжелые времена..

Retail sales in 1992 totaled $2.0 trillion. By 2011 they had grown to $4.7 trillion, a 135% increase in nineteen years. A full 64% of this rise is solely due to inflation, as measured by the BLS. In reality, using the true inflation figures, the entire increase can be attributed to inflation. Over this time span the U.S. population has grown from 255 million to 313 million, a 23% increase. Median household income has grown by a mere 8% over this same time frame. The increase in retail sales was completely reliant upon the American consumers willing to become a debt slaves to the Wall Street bank slave masters. It is obvious we have learned to love our slavery. Credit card debt grew from $265 billion in 1992 to a peak of $972 billion in September of 2008, when the financial system collapsed. The 267% increase in debt allowed Americans to live far above their means and enriched the Wall Street banking cabal. The decline to the current level of $800 billion was exclusively due to write-offs by the banks, fully funded by the American taxpayer.

.....

Credit cards are currently being used far less as a way to live beyond your means, and more to survive another day. This can be seen in the details underlying the monthly retail sales figures. On a real basis, with inflation on the things we need to live like energy, food and clothing rising at a 10% clip, retail sales are declining. Gasoline, food and medicine are the drivers of retail today. The surge in automobile sales is just another part of the “extend and pretend” plan, as Bernanke provides free money to banks and finance companies so they can make seven year 0% interest loans to subprime borrowers. Easy credit extended to deadbeats will not create the cash flow needed to repay the debt. The continued penetration of on-line retailers does not bode well for the dying bricks and mortar zombie retailers like Sears, JC Penny, Macys and hundreds of other dead retailers walking. With gas prices soaring, the economy headed back into recession and the Federal Reserve out of ammunition